Thailand Bank tests Blockchain with IBM

Thailand bank tests blockchain to certify official documents. To do so, it is is working with the IBM company.

According to Reuters magazine, in fact, Kasikornbank wants to cut costs related to record keeping.

The bank is one of the most important in Thailand and it is looking to create a document certification service by next year.

Also, Kasikornbank is talking with other Thai banks with the goal of establishing new collaborations that could involve a few members of the national financial system. According to the current plan, other banks together with Kasikornbank could use the blockchain network to certify documents.

In a press release published back in April, Kasikornbank revealed its decision to study and test new technologies, including machine learning and the distributed ledger.

At the time, the Thai bank explained that blockchain is “a technology that offers other benefits, e.g., reducing costs and increasing cross-border settlement efficiency that can be verified”.

This news also represented a turn within the Thai country, as two years ago the specter of a bitcoin ban in Thailandia led to problems for the local exchange activity.

After that, Thailand decided not to ban digital currencies, but published a warning to its citizens about their use.

Open your free digital wallet here to store your cryptocurrencies in a safe place.

MasterCard Releases Blockchain API

MasterCard releases Blockchain API, an experiment to work on an emerging technology such as the distributed ledger.

So Visa won’t be the only credit card company to work on the blockchain.

But while Visa is releasing a B2B blockchain, MasterCard releases blockchain API with more collaborative objectives.

The MasterCard website now contains 3 APIs connected to its internal blockchain platform, including offerings based on smart contracts and payment settlement. Those APIs were created by MasterCard Labs, the innovation program of the credit card giant.

MasterCard blockchain lead Justin Pinkham explained that the company created the API platform in October to stoke interest among banks and merchants.

Pinkham explained to CoinDesk magazine:

“This is part of our initiative to publish experimental APIs from Mastercard Labs and give developers the chance to work on emerging technologies that haven’t yet been commercialized by us.”

Also, Pinkham explained that MasterCard company is continuing to work on technology use cases and it is looking for new partnerships that can be useful for the MasterCard’s business.

“We believe that there is a role of blockchain in the future of commerce. This future needs to be developed in partnership with banks, merchants and industry participants,” Pinkham commented.

This news is one of the most important for MasterCard company, who used to criticize bitcoin in the past.

But if MasterCard releases Blockchain API, this means that it is beginning to push some of the work done by its tech lab.

According to Pinkham it won’t be the last, as he said that the company is creating a new foundation for blockchain tech that will be focused on the distributed ledger use cases including inter-bank payments, trade finance, digital identity and also the exchange of know-your-customer information.

This work was possible also thanks to the new partnership between MasterCard and startups through its Start Path Global program, as well as 30 more blockchain-related patents that Pinkham explained the company submitted.

Open your free digital wallet here to store your cryptocurrencies in a safe place.

IBM Blockchain to solve delivery issues

Singapore startup FreshTurf is working on a IBM Blockchain project to develop a network for solving issues related to delivery and storage lockers.

According to a press release, the two companies wants to create a network to track delivery shipments and storage lockers through the blockchain with the objective of providing a faster and safer service to the customers.

This way, in fact, users will be able to track their packages more easily thanks to a distributed ledger platform.

This is not the first project for the IBM’s BlueMix garage, a wordwide network of innovators that provides a hub for startups and companies to test and study the blockchain.

The BlueMix is a part of IBM blockchain broader strategy for fintech applications.

The two companies commented in a press release that their goal is providing a system for clients to check the status of their packages in real time.

“Not only can the application of blockchain technology help provide visibility across the fulfilment chain, allowing users to track their parcel and delivery status from the convenience of their phone, it can help stakeholders to conduct shipping transactions in a highly secure and trusted environment.”

This distributed system, currently in development, works through the IBM blockchain.

It is not still clear if the companies will sell the technology for commercial use.

IBM Blockchain and Australian Postal Service

Blockchain has been used for several use cases, including package delivery.

In fact, Australian Postal Service released a report explaining how they could use the distributed ledger to track packages movements. Read more about Australian Postal Service new project by clicking here.

Also, US Postal Service discussed its idea to create a new digital currency called PostCoin.

And this is not the first time IBM works on a blockchain-related project. Read more news about the IBM Blockchain here.

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Illinois Blockchain Strategy: a new working group

The U.S.A. State has created a new Illinois Blockchain Working Group for integrating the technology within the government.

This working group, created at the beginning of 2016, includes several representatives from public agencies, including the Department of Innovation and Technology, Department of Financial and Professional Regulation and the Department of Insurance.

Its main goal is identifying how the distributed ledger can improve government services and making it easier for users doing business with State agencies.

Director of the state’s Department of Insurance, Anne Melissa Dowling says her office is involved in a strong education campaign, to be the first agency in the U.S.A. to use the blockchain.

“Right now we’re trying to determine if we become a first mover in this space by developing a distributed ledger vision for government. But we’re doing a lot of listening and learning.”

During an interview, she explained that the distributed ledger can be used to make it easier relationships among Illinois insurance companies, regulators and policy holders.

So, the state wants to explore how the ledger can help to speed up this process.

“In concept its an absolutely beautiful thing. But we need to have a little more experience we need to spend a little more time with the data.”

Illinois Blockchain and Regulators

William Mougayar, author of “The Business Blockchain”, said that a semi-private blockchain developed by the state would be a strong basis to welcome in market stakeholders. According to him, the real challenge will be getting regulators on board, or the National Association of Insurance Commissioners.

“I suspect that the regulatory aspect is a more critical hurdle that will need to be addressed,” he said.

At the moment Dowling and her group are still thinking about the options they have. She explained that she studying the technology and its potential use cases for her agency, so she’s still learning more and more about the blockchain.

As part of that process, Dowling will participate in a blockchain regulatory panel held in Chicago on November 8th and she says that her first goal will be learing as much as possible.

Also, Dowling comments she is observing working models that can explain how blockchain can be implemented in insurance groups.

These were here words:

“These efforts are really on behalf of consumers to ensure we can serve them in the most efficient and cost-effective way. Illinois wants to look at everything possible to achieve that goal.”

Credit: Coidesk.com

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Blockchain Insurance: applications for insures

Five major European companies will work on a blockchain insurance project to provide faster and safer services to their clients.

This project, called the Blockchain Insurance Industry Initiative (B3I), has the goal of testing use cases that could help the insurance sector.

To do so, in fact, Allianz, Aegon, Munich Re, Swiss Re and Zurich, or the biggest companies of this field, are working to provide a meeting ground to exchange ideas with this objective: improving the insurance service and creating a new method of doing business.

“We want to be at the heart of these developments and see Blockchain as one of those potential catalysts for change. By actively creating partnerships and making strategic investments we can build smarter solutions together with our clients,” explained Mark Blook, chief technology officer at Aegon.

Allianz – which has already explored smart contracts for catastrophe bonds exchange and has already worked with fintech startups – belives that the distributed ledger can allow them to help transparency for their users.

“This initiative, enabling alternative operating models based on the Blockchain technology, can help us increase transparency and efficiency and deliver a better experience to our customer,” commented Allianz Group COO Christof Mascher.

Those 5 companies said they hope that other brands in the insurance and reinsurance industries will join the project with them.

According to a press release, the mai objective is taking advantage use cases “across the entire insurance value chain”.

Open your free digital wallet here to store your cryptocurrencies in a safe place.

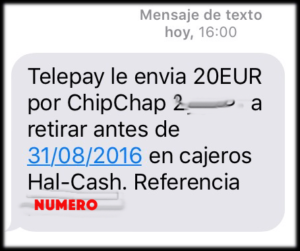

Bitcoin euro: withdraw with ATM machines

Holytransaction Trade is a new platform offered by HolyTransaction wallet for Bitcoin Euro instant conversion.

Holytransaction.trade is useful when you want to convert your bitcoin into euro, by using any ATM machine with Halcash that you can find in Spain and Poland.

Thanks to HolyTransaction Trade you can do this operation in a few minutes, without having to wait a few days as if you use traditional exchanges.

Anybody can convert his own bitcoins into euro from an ATM machine with Halcash, whether he has a wallet on HolyTransaction or not.

Where is the service available?

The Halcash service is available only in Spain and Poland at the moment.

How much fees?

To convert bitcoin into euro with Halcash, this platform holds a 2% fee.

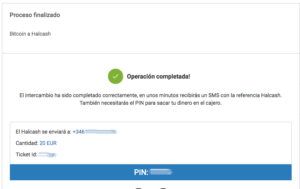

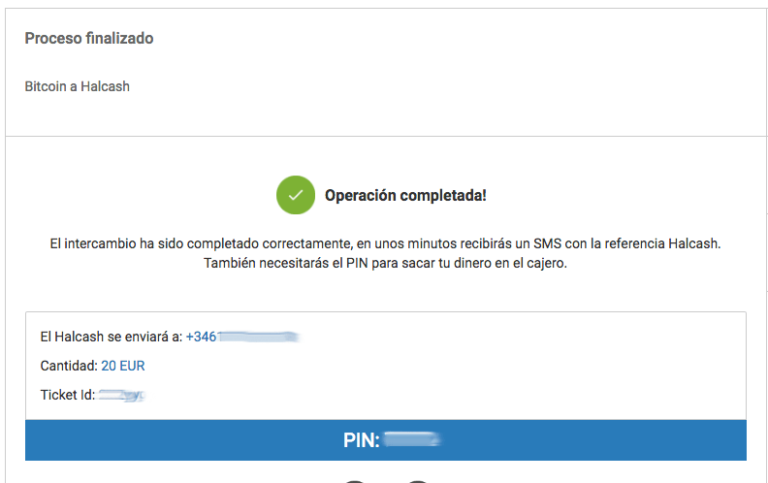

How does it work? Bitcoin Euro instant conversion

Here you can read a step-by-step guide to convert your bitcoin into euro by using HolyTransaction Trade and the 10.000 HalCash ATM you can find in Spain (or Poland).

- Go to Holytransaction.trade website

- To do a transfer from Bitcoin to Halcash you need to select “Bitcoin” on the right and “Halcash” on the left. Then, click on “Continue”.

- Select an amount and your telephone number where the system will send a verification code.

- Follow the instructions and open your wallet to do a transaction to the address on the screen. Of course, you need to send the same amount you selected in the previous window.

- Once you did, the transaction will be confirmed on the blockchain and you’ll receive a message on your mobile with the password to withdraw your funds at a Halcash ATM.

- Then go to a Halcash ATM, enter your password and withdraw your euro. You need to fill all the fields with mobile number, amount, password, reference number (you received it on your smartphone).

- You can withdraw your amount. This whole operation takes only you a few minutes.

Download the HolyTransaction App here for free.

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Philips announces its own Blockchain Lab

Previous Statement

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Ethereum used for Car Charging in Germany

Germany supports green power

Car Charging with Smart Contracts

Open your free digital wallet here to store your cryptocurrencies in a safe place.

9 Best Bitcoin Video Animations

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Bitcoin is “digital gold” and will mark the end of cash. Ametrano from IMI Bank explains.

Bitcoin is a private currency, that isn’t issued by any central bank nor guaranteed by any institution. It is electronically transferrable in a practically instant way, utilising a cryptographic security protocol. It is based on a completely decentralized network: the transactions don’t require a middleman, cannot be censored, don’t have any kind of geographical or amount restriction, and are possible 24 hours a day every day and are substantially free.

Open your free digital wallet here to store your cryptocurrencies in a safe place.