European Central Bank hacked, personal data stolen

Open your free digital wallet here to store your cryptocurrencies in a safe place.

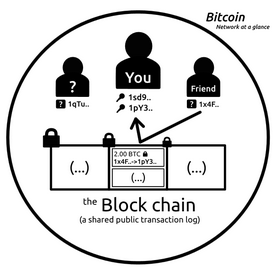

Think the Internet’s disruptive? Hold tight for blockchain!

This matters because, as Sparkes sets out under his provocative headline of The coming digital anarchy,

this is a system that can be applied not just to money but to any kind of transaction, from domain name registration to legal arbitration or public elections. In between those two extremes, it could completely overturn the way enterprises organize themselves and tout for business.

Where’s the distributed, anonymous, permission-less system for chatty machines to allocate their scarce resources? Where is the ‘virtual money’ to create this ‘virtual economy?’ …

Someday, they will be used by the machines in our network, on our desk, in our garage, and in our pocket to exchange value and achieve consensus at blinding speeds, anonymously, and at minimal cost.

What Ravikant is really describing here is not Bitcoin per se but the work of the blockchain, providing a trusted, shared transaction record that allows machines to own and exchange value without human intervention. Although in strict engineering terms it’s not really a protocol, its impact is potentially as huge as any of these other building blocks of the Internet.

Effectively, Ravikant is arguing the blockchain is how the Internet of Things will exchange value — not just monetary value, but also many of those other components of business transactions that we currently find much harder to quantify, such as trust and reputation.

Autonomous things

Now back to Sparkes, who recounts a scenario imagined by Mike Hearn, an ex-Googler who now works on Bitcoin:

Far-fetched it may be, but this is the kind of scenario that is getting venture investors excited about blockchain right now — and you can understand why.

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Bitcoin like the Internet In 1995

is receiving more venture capital investment than early stage Internet

companies were in 1995. Remember what the Internet was like in 1995?

looked like. If not, the piece discusses how hard it was to stream

video, how there was no safe way to process credit cards, how ugly the

websites looked and how slow the Internet was.

anyone uses it, it isn’t safe, and it is hard to use. However digital

currencies are so much cheaper, more convenient and more powerful than

their analog counterparts that, like the Internet, their widespread

adoption seems assured.

competing digital currencies have entered the market. So far none has a

clear shot at overtaking bitcoin. Bitcoin’s network effect is growing at

a fast rate, making its dominance even more likely.

Open your free digital wallet here to store your cryptocurrencies in a safe place.

A little altcoin sanity: Peercoin

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Under the microscope: conclusions on the costs of Bitcoin

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Bitcoin: Education can make a difference

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Bitcoin: the future of payments

Payments networks revisioned with bitcoin

Why bitcoin is held back

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Google update now supports Bitcoin price in search results!

“You can also ask Google to do conversions – if you have the Google Search app on your smartphone, for example, ask it, ‘How many bitcoin are in 500 U.S. dollars?’ and you’ll get the answer in a handy conversion tool.”

Open your free digital wallet here to store your cryptocurrencies in a safe place.

The line between fiat and cryptocurrency is getting fuzzier.

(BitcoinMagazine) The line between fiat and cryptocurrency is getting fuzzier. With the advent of Bitcoin 2.0 technology, we can now use cryptocurrency to exchange stocks, property, commodities, and even state-backed money. But if the whole point of cryptocurrency was to decentralize the financial system, what’s the point of a dollar-backed coin?

Dollar-backed digital coins have been attempted many times before. The Canadian government even tried to get in on the action, and unsurprisingly failed. Some claim that the first cryptocurrency to attempt this was Coinaaa, but this is technically incorrect. Coinaaa sells premined coins, and does invest a lot of the revenue in Norwegian krone, but their intention is to maintain a stable value independent of any state-backed currency. The company invests their earnings, and uses some of the money to buy back coins when the price drops, or sell coins when it rises.

The company promises 0% transaction fees, but at the cost of a centralized mining system. While this fails to represent actual kroner one could trade in a decentralized manner, it does serve as a great transactional currency. This is theoretically possible without having to rely on humans–decentralized autonomous software could do this by adjusting block rewards or destroying transaction fees in response to price fluctuations–but if they make the right investments, it functions for now.

Given the possible and existing options available, one might then wonder why Brock Pierce chose to introduce Realcoin, the first cryptocurrency backed by US dollars. Although they claim to hold US dollars in “conservative investments,” this probably means they’re doing the same thing Coinaaa is with your money. The major difference is that they aren’t trying to maintain a stable value: Realcoin claims they will maintain a fully-auditable 1-to-1 reserve of US dollars, which can be redeemed for their coins. This is all enabled by the Mastercoin protocol (Omni Layer) on the existing Bitcoin blockchain.

This will cause Realcoin to fluctuate with the value of the dollar, for better or for worse. It will inflate with time, as all fiat money does, meaning you won’t want to keep your savings in it–Bitcoin would be a better choice. A good transactional currency should be neither inflationary nor deflationary, so Coinaaa is clearly the superior choice for daily use; both will likely make their profit by trading and investing with your money, and require very similar amounts of trust.

Why, then, create Realcoin? Although the Coinaaa company will definitely hold some kroner, a Coinaaa will not represent the value of a Norwegian krone. This means that if you want to do FOREX trading involving Norwegian currency, you have no choice but to return to centralized exchanges. Even if you don’t want to hold or use kroner, there’s profit to be had in exchanging it.

Realcoin, therefore, represents an opportunity to speculate with fiat currency for the first time. If you have reason to believe its price will move for or against a digital currency on the market, now you can take advantage of that. Given that the Mastercoin protocol will almost certainly contain a decentralized exchange, Realcoin allows you to trade in US dollars without ever touching a traditional financial institution. The state is just like any other company, issuing money that you can choose to use–or not.

Open your free digital wallet here to store your cryptocurrencies in a safe place.

LinkedIn co-founder: Bitcoin is in my five-year Investment plan

In the interview, Hoffman discussed his personal experience with bitcoin, confirming that he has purchased “a few bitcoins” to date in addition to his investment in Xapo.

In the interview, Hoffman discussed his personal experience with bitcoin, confirming that he has purchased “a few bitcoins” to date in addition to his investment in Xapo.Open your free digital wallet here to store your cryptocurrencies in a safe place.