BTC China in discussion with regulators over Bitcoin recognition

(CoinDesk) The world’s busiest bitcoin exchange, BTC China, has been in talks with regulators to approve bitcoin as an official currency, according to Bloomberg Businessweek.

While there have been some ‘lower-level’ discussions, the company has not yet had any success arranging high-level meetings, said BTC China CEO, Bobby Lee.

This isn’t surprising, given the reluctance of governments worldwide to make official statements about the currency’s legal status.

To grant official approval would likely cause a spike in activity, with many fearing activity on such a grand scale could undermine one of government’s key economic powers: overseeing fiat currencies. This hasn’t stopped a recent flurry of interest from high-level government officials, as bitcoin’s value soars too high to ignore. At the time of writing, the bitcoin price on BTC China was 6,267 CNY, or $1,027. Mt. Gox’s price was $1,050, and it was around $990 on the Coindesk BPI. The upper echelons of government feature many opinions on bitcoin, including some that have shifted over the years. Senator Chuck Schumer, who in 2011 described bitcoin as “an online form of money laundering,” and called for a crackdown, recently tweeted that the cryptocurrency had “significant potential”. Deputy governor of China’s People’s Bank, Yi Gang, hinted at a personal (unofficial) approval of bitcoin exchanges and people’s ability to trade in and out of digital currencies, but also said it would be impossible for the central bank to recognise bitcoin “in the near future”.

BTC China has taken Gang’s comments on board, and Lee has continued to hold discussions with local regulators. He has also answered questions about how bitcoin should be regulated, remaining optimistic about the long-term, describing bitcoin’s current status as:

“Not on the black list and not on the white list. It’s in the grey area.”

In the bitcoin universe, anything short of a call for blacklisting can be taken as progress. But while its “grey area” status allows exchanges and payment processors to function reasonably well at the moment, many think some form of recognition and subsequent regulation is necessary for bitcoin to gain widespread acceptance.

Open your free digital wallet here to store your cryptocurrencies in a safe place.

British Island wants to make physical Bitcoins with UK Royal Mint deal

(CoinDesk) A tiny island in the English Channel, Alderney, wants to mint physical bitcoins as part of a larger campaign to become one of the world’s first financial services centers devoted to digital currency.

The Financial Times reported

that Alderney, just three miles long with a population of 1,900, wants

to become known as an international center for bitcoin transactions.

Intended to be fully compliant with anti money-laundering and other

financial regulations, it would offer merchant payment services,

exchanges, and a bitcoin storage vault of some kind.

The physical

bitcoins, like other such tokens, would be collectors’ items rather than

circulated, and would likely have a gold content (apparently around

£500 worth) to further their appeal and allow them to retain value

should bitcoin’s price crash.

They would also serve as promotional

tokens for the more ‘serious’ bitcoin payment and exchange services.

Alderney’s

coins would hopefully be minted in a collaboration with the UK’s Royal

Mint as part of a commemorative collection. Rather than having a private

key sealed inside, like the popular Casascius physical bitcoins

and their contemporaries, the Alderney bitcoins would be exchangeable

for the more useful digital kind by its holder paying a visit to the

island. They would not be official legal tender otherwise.

Production

would be overseen by an independent company, who would also take the

hit if bitcoin’s value vanished. The same company would also hold the

coins’ keys in an escrow service. If the deal goes ahead, The Royal Mint

would handle orders and take some of the money from sales.

With current bitcoin values hovering around $1,100 on CoinDesk’s BPI

(over $1,200 on Mt. Gox) and seeming to jump higher with each passing

day, more daring segments of the financial world are sensing an

opportunity to create a whole new industry. The high values, including

not only bitcoin’s but those of other digital currencies

as well, are wrenching the concept out of the hands of tech-savvy

entrepreneurs and delivering it to people more accustomed to

billion-dollar movements.

Bitcoin and digital currencies, despite

occasional murmurings and investigations by authorities, still have no

legal recognition as currencies in any major jurisdiction. No

legislation has been tabled specifically for digital currencies, though

exchanges and payment processors generally fall under the same

know-your-customer (KYC) and anti-money laundering (AML) regulations as other ‘money transmitters’.

The

Channel Islands, just off the coast of France, are ‘Crown Dependencies’

and not officially part of the UK. This special legal status has

traditionally made them a hub for offshore financial services, with most

of the activity happening on larger Guernsey and Jersey.

Alderney falls under the jurisdiction of the Bailiwick of Guernsey

but has been looking for ways to gain more financial independence from

its neighbors. The island has long produced stamps and minted its own

coins, called the Alderney pound, pegged 1:1 to UK pound sterling. The

coins are produced in denominations of £1, £2 and £5 in ordinary

cupro-nickel as well as gold and silver versions, and are also aimed

primarily at collectors.

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Bitcoin in the UK: HMRC suggests bitcoins are ‘taxable vouchers’

As Tom Gullen described on his blog, Her Majesty’s Revenue & Customs (HMRC) seems to be classifying bitcoins as vouchers, which means VAT would be due on any sales. A 20% mark-up on bitcoin prices would make UK exchanges untenable. In addition to Gullen’s statement, an independent source told us that HMRC had given them the same classification. We also spoke to Dr Tom Robinson of the UK-based bitcoin exchange BitPrice and consulting firm Blockchain Consulting, who recently attended the Financial Innovators Summit at 10 Downing Street. At the time, it was said that he “left the meeting feeling largely optimistic”. However, his subsequent communications yielded the following statement from HMRC: “Our Policy teams’ view is that these are not currency. It is our view that the provision of bitcoins is the sale of vouchers. These arelikely to be ‘single purpose’ vouchers.”

Robinson said: “This is obviously an entirely inappropriate classification for

bitcoin: they aren’t issued by anyone, they don’t have a ‘face value’

and they can be redeemed for a wide range of goods and services.”

Robinson also posted to reddit, saying: “We do now have a commitment from the Treasury that they will seriously consider how bitcoin might achieve official recognition in the UK. In doing this the government is seeking input from bitcoin businesses.” Any businesses that want to submit a comment should do so through this link. HMRC told CoinDesk that “There is a VAT exemption for currency transactions but the currency in question must be legal tender. We will of course listen to arguments for alternative VAT treatments under existing VAT law.”

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Korea announces favorable tax policy for Bitcoin

The bitcoin community in Korea is small, but growing, and it seems that governments around the world are taking the US Senate’s recent hearings as a signal to begin determining at least temporary policies regarding our favorite cryptocurrency.

Posted in Korea’s Bitcoin Community on Facebook is a statement from Korea’s National Tax Service stating that Koreans will not be taxed for capital gains on bitcoin for the time being.

While this is clearly good news for the few long-time miners in Korea as well as speculators that have experienced a windfall in the past month, it is important to remember that this is not a good long-term position toward bitcoin. Essentially, the Korean government is taking the stance that bitcoin investments are not real.

Currently, bitcoiners are happier to be left alone by the governments of the world and such a policy supports this in the long term. But if we hope to see bitcoin rise to a more commonly-accepted and competitive currency, we will need governments to recognize that BTC does, in fact, bear value and follow “safe and sane” regulatory procedures. While this is not the time to hold the argument over how much and what kind of regulation would be appropriate and positive, I think that most bitcoiners will agree that we don’t want it to be seen as monopoly money forever. Near-universal recognition and respect is needed.

Open your free digital wallet here to store your cryptocurrencies in a safe place.

This Senate hearing is a Bitcoin lovefest

(WashingtonPost) The Senate Committee on Homeland Security and Governmental Affairs,

chaired by Sen. Tom Carper (D-Del.), is holding the first congressional

hearing on the future of Bitcoin. The first panel features senior

figures from the Obama administration. And their comments about Bitcoin

have been remarkably positive.

After the officials gave their opening statements, Carper’s first

question drew a parallel to the Internet. He pointed out that in the

early days of the Internet revolution, many people raised concerns about

illicit use of Internet technologies. Yet in the long run, he argued,

the Internet has had a hugely beneficial effect on peoples lives, making

possible previously unimagined services like Facebook and YouTube.

Carper wanted to know if the witnesses saw Bitcoin in the same light.

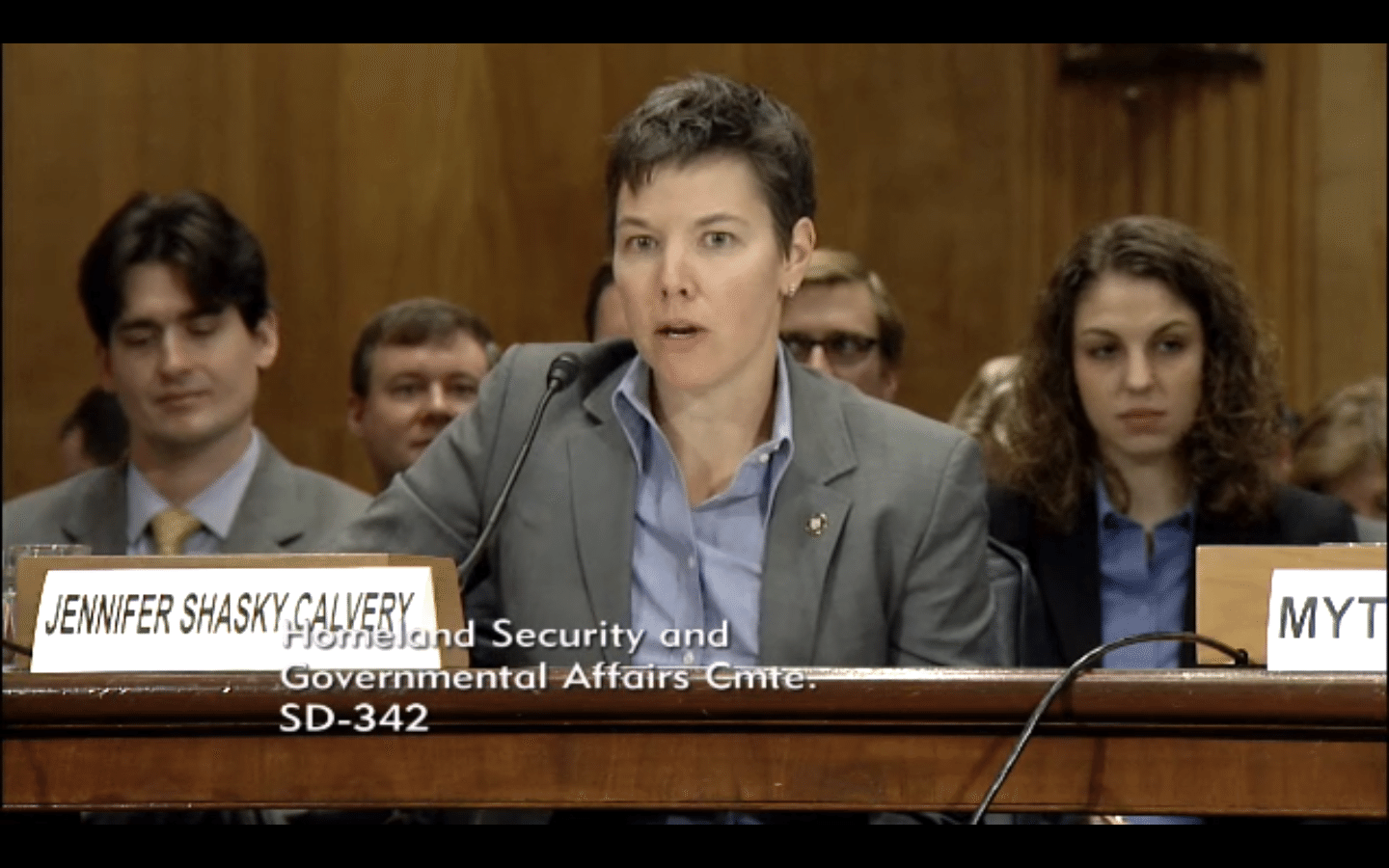

Jennifer Calvery, director of the Financial Crimes Enforcement

Jennifer Calvery, director of the Financial Crimes Enforcement

Network, agreed with Carper. “Innovation is a very important part of our

economy. It’s something for us to be proud of,” she said.

“We are attuned to the criminal use,” added Mythili Raman of the

Justice Department. But “there are many legitimate uses. These virtual

currencies are not in and of themselves illegal.”

“There is good reason for us to remain watchful” about Bitcoin being

used for illicit purposes, Raman added. “But we also intend to balance

that against the need for legitimate users” to use the technology.

Later in the same panel, Edward Lowery of the Secret Service

testified that cyber criminals “have not by and large gravitated toward

peer-to-peer cryptocurrencies.” Rather, they “have by and large

gravitated toward centralized digital currencies that are based in a

locale that may have less regulatory guidelines and less aggressive law

enforcement.”

That’s been the tenor of the entire hearing so far. All three Obama

administration officials expressed concern about Bitcoin being used for

illicit uses. But they also stressed that Bitcoin has important

legitimate uses and that regulators need to be careful not to stifle

innovation in virtual currencies. And they seemed to believe that the

situation was under control, and none asked for new regulatory powers to

crack down on illicit uses of the currency.

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Bitcoin price skyrockets as Senate hearing concludes

(CoinDesk) The price of bitcoin spiked dramatically last night and the

transaction volume on the Bitcoin protocol (in USD) eclipsed that of

Western Union.

The spike took place after Jerry Brito, Patrick

Murck and Jeremy Allaire presented their testimonies on bitcoin and the

future of virtual currencies to the Homeland Security and Governmental

affairs committee in the US senate at the Senate hearing titled Beyond Silk Road: Potential Risks, Threats and Promises of Virtual Currencies.

The CoinDesk BPI read $650 on conclusion of the hearings, with Mt. Gox reporting a jump to $750 and, later, BTC China reaching a record high of 6,989 CNY (approximately $1,147) before crashing to almost 60% of this value in seconds, and then recovering to about $850. At the time of writing, the CoinDesk BPI puts the price at $602.

The

senate hearing is being hailed as an historic moment for bitcoin, with

even Ben Bernanke, current chairman of the Federal Reserve remarking

that virtual currencies “may hold long term promise” in an open letter

to Senator Thomas Carper (D) published 12th November.

At the

hearing, Senator Carper listened to commentary, criticism and praise of

bitcoin with a temperament that left many in the bitcoin community

impressed and even delighted, whilst Jennifer Shaskey Calvery from

FinCEN was measured in her analysis and assessment of the promises and

threats that virtual currencies present.

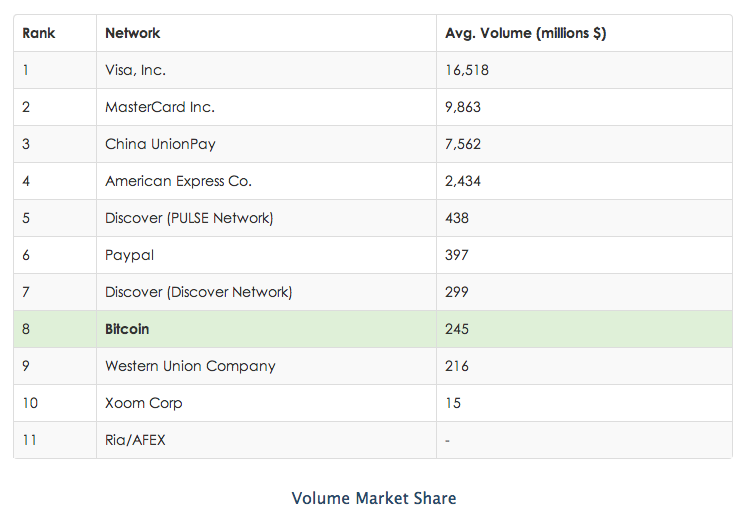

This morning, data analysis website Coinometrics reported

that bitcoin passed Western Union in daily transaction volume,

transacting an average of $245m compared with Western Union’s estimated

$216m but is still behind on the average number of daily transactions at

approximately 62,000, with Western Union clocking up approximately

633,000 transactions per day by comparison.

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Bitcoin skyrockets to $600 after U.S. agencies label it legitimate

(DailyDot) The Department of Justice and Securities and Exchange Commission told senators that bitcoins are “legitimate financial instruments,” Bloomberg reports. The news comes just three days ahead of a U.S. Senate Committee on Homeland Security and Governmental Affairs hearing on Bitcoins,

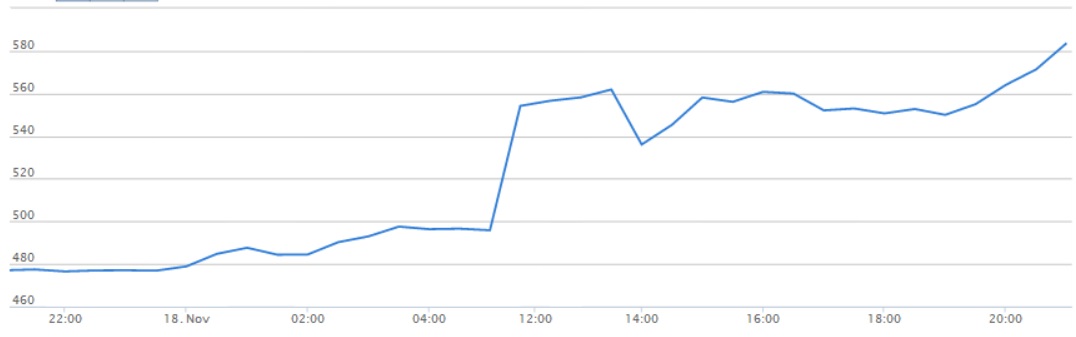

Almost immediately following the article publication at 12:01am ET, the

average price of Bitcoins jumped over $50, from $495 to $554, sprinting

past the $500 milestone. It has continued to climb to a $583 average in the hours since. At Mt. Gox, the largest Bitcoin exchange, the currency is already selling for $630.

The Senate committee, which was scheduled immediately following the fall of the Deep Web black market Silk Road, aims “to explore potential promises and risks related to virtual currency for the federal government and society at large.”

“The FBI’s approach to virtual currencies is guided by a recognition

that online payment systems, both centralized and decentralized, offer

legitimate financial services,” Peter Kadzik, principal deputy assistant

attorney general, wrote according to Bloomberg.

“Like any financial service, virtual currency systems of either type

can be exploited by malicious actors, but centralized and decentralized

online payment systems can vary significantly in the types and degrees

of illicit financial risk they pose.”

Ben Bernanke, the chairman of the Federal Reserve, said he had no plans

to regulate the currency. In fact, Bernanke isn’t sure if the Fed even

has the authority to do so.

In an article on Sunday, Time reported that the Senate hearings were “just the beginning.”

“Honestly, the environment seems to be a game of hot potato where no

politician wants to be caught being pro or anti bitcoin,” Charles

Hoskinson, director of the Bitcoin Education Project, told the magazine.

“Once the market cap gets to around $10 billion or so, then expect real

hearings and a lot of lobbying.”

At nearly $7 billion and triple what it was just two weeks ago, the cap is closing in fast on Hoskinson’s milestone.

The reaction in the Bitcoin world has been ecstatic. After similar reports of Chinese authorities saying the government has no plans to

regulate the digital currency, news that the U.S. is following suit is

exactly what Bitcoin-backers had hoped for. Around the Internet, bitcoin

enthusiasts talked about the adrenaline they felt watching the price

surge this morning.

There is already widespread speculation in the community that the currency will soon enough reach $1,000—and beyond.

Open your free digital wallet here to store your cryptocurrencies in a safe place.

What exactly does the US government really think of Bitcoin?

(CoinDesk) With the US Senate setting 18th November as the start date for its committee hearings into bitcoin, it’s time to

take a look at some of the more significant events in bitcoin’s short but colorful legal history.

The early Bitcoin timeline featured hacks, heists, drugs, demands for refunds and the first appeals to law enforcement, but 2013 saw official scrutiny rise almost as quickly as bitcoin’s value.

{kind=link}

Whether or not bitcoin requires, or should seek, regulatory approval is a major source of heated debate on bitcoin discussion forums, but the regulation issue will remain prominent as long as significant amounts of wealth are at stake.

FinCEN issued guidelines that bitcoin-related businesses counted as “Money Service Businesses” (MSBs) under US law.

This meant bitcoin businesses were now officially required to provide authorities with information about potentially suspicious transactions and introduce policies to prevent money laundering. These regulations also affect the more centralized virtual currencies and point systems used in social networks and online games, including Facebook and Second Life. Lack of a centralized authority meant bitcoin itself could not comply, but any business associated with its use would need to — including individual miners, if they converted their bitcoin to fiat currency.

In something of a rare public compliment for bitcoin from the world of traditional finance, François R. Velde, senior economist of the Federal Reserve in Chicago wrote a glowing paper titled “Bitcoin: A Primer” in which he wrote bitcoin was a “remarkable conceptual and technical achievement, which may well be used by existing financial institutions.” He further described bitcoin as an “elegant solution” to the digital currency problem and claimed its value derived from certain beliefs about the nature and function of money, and the amounts of fiat currencies traded for it.

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Regulation Of Bitcoin – The European Bitcoin Convention — 2013 Amsterdam

Regulation Of Bitcoin at the European Bitcoin Convention

Wieske

Ebbe (Dutch Central Bank), Michael Maier (Fidor Bank), Niels Ploeger

(Amsterdam Police), Joerg Platzer (Crypto Economics Consulting Group)

& Casper Riekerk (Finnius Lawyers)

Recorded By IamSatoshi

Open your free digital wallet here to store your cryptocurrencies in a safe place.

US Homeland Security committee to explore bitcoin’s potential in 18th Nov hearing

Open your free digital wallet here to store your cryptocurrencies in a safe place.