What Dogecoin must do to survive

Tim Swanson is an educator, researcher and the author of ‘Great Wall of Numbers: Business Opportunities and Challenges in China’. Here, he explores the mining systems of dogecoin and litecoin to show how the dogecoin economy can thrive.

(CoinDesk) The key ingredient to the success of any decentralized public ledger, such as bitcoin, is incentivizing its transactional network to simultaneously secure the network from attackers and process transactions.

In the case of bitcoin, and in the case of virtually all other cryptocurrencies, this incentivization process is handled through seigniorage. Every 10 minutes (or 2.5 minutes for litecoin, or one minute for dogecoin) a fixed amount of bitcoins is paid to the labor force called “miners.” These miners are computational systems that perform never-ending mathematical calculations dubbed hashing. This hashing in turn creates security for the network; so as long as more than 50% of the hashrate is maintained by “good” systems, bad actors are prevented from manipulating the ledger.

The other key role these miners also fill is processing and including transactions into packages called blocks. Every 10 minutes, one miner is rewarded for processing these blocks with fixed income. Last month David Evans published a good overview of how this process looks from a labor input and supply output perspective.

For some advocates, one of the purported advantages of cryptocurrencies is that their money supply creation rate is actually deflationary (or contractionary) in the long run – in the short run, bitcoin’s expansionary rate is quite high, with inflation at 11.1% this year alone. That is to say, it is a hardcoded asymptote, tapering off over a known time period. In the case of bitcoin, the wage for the labor force (miners) is split in half roughly every four years (every 210,000 blocks), for approximately the next 100 years – until its money supply is exhausted at a final 21 million bitcoins.

Roughly 12.7 million bitcoins have already been paid to miners. With dogecoin’s 100 billion dogecoins, this process is accelerated, with the mining income dividing in half every two months. While it took about five and a half years for about 60% of bitcoin’s total monetary base to be distributed, as of today 78% of dogecoin’s reward (income) has already been divvied out to its workforce in less than six months.

What now for the workforce?

While this frenetically fast money supply has provided a psychological motivation for early adopters to partake in the dogecoin ecosystem, economic law suggests that this network will probably cease to exist in its current form within the next six months probably through a 51% attack.

The reason is simple: with every block reward halving, also called “halvingday”, the labor force is faced with a 50% pay cut. The contractors (laborers) incapable of profitably providing hashrate at this level can and will leave the work force for greener pastures. This same issue has impacted other altcoins in the past, such as MemoryCoin, which died after nine months due to a combination of factors including diminished block rewards (it attempted to divvy out its entire monetary supply in two years).

Early advocates of dogecoin like to point to outlier events such as the Doge bobsled team or sponsored NASCAR driver at Talladega or even a vaunted tipping economy (which is actually just faucet redistribution) as goal posts for growth and popularity, yet after two halvingdays the actual dogecoin block chain has lost transactional volume each month over the past four months and the labor force has also left for new employment elsewhere.

This is visualized in the following two graphs.

The first chart shows dogecoin’s collective hashrate. The black lines indicate when the “halvingday” or rather “income halvingday” occurred. Because the price level of a dogecoin remained relatively constant during this time frame, there was less incentive for miners to stay and provide labor for the network. If token values increased once again, then there may be incentives in the short-term for laborers to rejoin the network. Yet based on this diagram, roughly 20-30% of the labor force left after each pay cut.

The second chart shows on-chain transactional activity. The first three months are erratic because of how mining pools (similar to lottery pools) paid their workforce (miners). Following the first halving day in February, the network transaction rate fell to roughly 40,000 transactions per day and then leveled off to around 20,000 until 28th April 2014, when another halvingday occurred and the subsequent transactional volume remained relatively flat to negative. It is currently at 12,850 transaction per day, or roughly the same level it was during the first week of its launch five months ago.

Dogecoin’s falling hashrate

Now, some readers may claim that a lot of the transactional volume such as tip services and tip bots are being conducted off-chain and thus the total number of transactions is likely higher. And they would be correct. But that would completely defeat the purpose of having a block chain in the first place – a trustless mechanism for bilateral exchange that negates the need for “trust-me” silos (as Austin Hill calls them).

Also, while this topic deserves its own series of articles, there is little literature that suggests that tipping can grow

an economy; it is not a particularly good signaling mechanism or way to grow a developing economy (i.e., “China, you need more tipping activity to grow and prosper”).

However the key issue is this: if the trend continues and the network hashrate continues to fall 20-30% after each halvingday, then within the next two to four months it will be increasingly inexpensive for competing mining pools on other ledgers to conduct a 51% attack on dogecoin’s network, destroying its credibility and utility.

For instance, the chart below is the litecoin hashrate over the past six months. Litecoin is dogecoin’s largest competitor based on its proof of work (PoW) mechanism called scrypt:

One of the reasons the litecoin hashrate is not rising or falling at a constant rate but is instead jumping up and down erratically is that miners as a whole are economically rational actors. When the cost of producing security is more than the reward (block reward income), the labor force turns towards a more profitable process such as another alternative scrypt-based “coin” (note: bitcoin’s hashing method uses SHA256d whereas litecoin and dogecoin use scrypt). The same phenomenon of hashrate jumping up and down occurs with the bitcoin network.

For the sake of simplicity, the litecoin network can be viewed as roughly 200 GH/s versus the dogecoin кошелек network which is roughly 50 GH/s. To conduct a 51% attack on dogecoin today, an entity would need to control roughly 25-26 GH/s which is roughly one eighth the processing power of the litecoin network. The current ‘market cap’ for dogecoin is $35 million, assuming marginal value equals marginal cost, ceteris parebus on paper it could cost $17.5 million in capital and operating expenses to successfully attack the dogecoin network.

The chart above shows both the hashrate of litecoin (in red) and dogecoin with the vertical black lines representing the dogecoin “halvingday.” What this shows is that while dogecoin, for roughly one month in early 2014 was more profitable to mine than litecoin, the halvingday led to an exodus of labor.

If current prices and trends continue, which they may not, in two months the litecoin collective hashrate may hit 240 GH/s and dogecoins hashrate could shrink due to halvingday by another 20% to 40 GH/s. At this rate a successful 51% attack on dogecoin would require just one twelfth of the hashing power of litecoin which at the same prices levels would entail less than $10 million in capital and operating expenses to do.

Will dogecoin survive?

While the development team could theoretically switch its proof of work algorithm (to X11 as used in Dash), the doge community is really faced with six options:

- Merge mine. Namecoin was (and is) an independent block chain, but since block 19,200 about 80-85% of its network hashrate (and block rewards) are tied to bitcoin mining pools through a process called “merged mining.” The new sidechains project from Blockstream is attempting the same process. Charlie Lee, creator of litecoin explained how dogecoin could be “merged mined” with litecoin in a series of posts last month.

- Transaction fees. Both the development team and mining community could agree to float or raise transaction fees on the doge network, similar to what Mike Hearn has been discussing for bitcoin. In practice however, even if approved, very little actual commerce, and therefore transactions, is conducted on the dogecoin network. Thus it is unlikely that this will compensate the large drop in mining income. Similarly, as Gavin Andresen pointed out in Amsterdam this past Friday, increased transaction fees reduces the participation rate. It is important to note the actual transaction costs are much higher than stated – block rewards (token dilution) are usually not factored in.

- Proof of stake. There are several variations of proof of stake. Whereas bitcoin, litecoin, dogecoin and most other cryptocurrency experiments use a “proof of work” mechanism to protect the network from malicious entities, a proof of stake system, such as that used in NXT, will randomly assign a “mining node” called a “forger” – a poor marketing term for sure – to process all the blocks for the next minute. Because all of the other nodes in the network know which miner to trust, this lowers the amount of infrastructure needed to protect the network. In theory this sounds amazing. In practice however, most proof of stake systems end up almost immediately centralized in one manner or the other. Andrew Miller, Andrew Poelstra and Nicolas Houy call it “proof of nothing”. Perhaps Stephen Reed’s version can work in the future.

- Increase in market price. This would incentivize the labor force to continue providing security of the network with the expectation that the tokens they are given in return for their labor will continually appreciate in value. This is betting on hope. Charlie Lee pointed out the uphill task this would require beginning next year when rewards fall to less than one tenth what they are today, stating last month, “At dogecoin block 600,000, only 10,000 coins will be created per block. So in order for dogecoin to keep the same amount of security as today, dogecoin price would need to go up by 25 times. And dogecoin price would need to gain on litecoin by 50 times in order to catch up on litecoin’s security. And assuming everything stays the same, the market cap of dogecoin needs to reach $1.5 billion by January of next year.” For comparison, the ‘market cap’ of dogecoin today is roughly $35 million (note: it is probably not accurate to call it a ‘market cap,’ see Jonathan Levin’s explanation).

- Migration. Dogecoin could also migrate to a platform like Counterparty and become a fully secured altcoin with a dash of proof of transaction thrown in to inflate the coin with ongoing usage that this particular community likes to embrace. It could be fully protected by the bitcoin hashrate with no further need to try to acquire miners to protect it.

- Further experimentation. While it is unlikely the dogecoin has the resources to create secure production code in the shortened time frame, Robert Sams “growthcoin” and Ferdinando Ametrano’s “stablecoin” could provide a mechanism that enables the network to live on in a different manner.

While any or all of these may be tried out, it may be too little, too late. With that said, stranger things have happened. A rising tide lifts all boats and thus in the event that “bitlicense” approved exchanges on Wall Street come online this summer and new capital actually flows into bitcoin and other alternative ledgers, perhaps similar speculative funding will flow into dogecoin as well. However, this is not something that can be known a priori.

I contacted Jackson Palmer, creator of dogecoin for his thoughts on the situation. In his view:

“It is definitely a challenge that dogecoin (and all current-gen crypto currencies) will face in the future. As we discussed recently, it’s kind of a sad reality that people are purely profit driven and these decentralized networks we’ve built are reliant on profit-mongers to power and secure their viability. I’m very concerned about the impact of centralized mining and reliance on transaction fees could hold for bitcoin as it becomes less enticing to mine – really, the network can be held at ransom to attach hefty transaction fees if the mining pools are cherry picking as they create blocks. At the end of the day, I think the viability of cryptocurrency really hinges on a move away from PoW-based mining to something new and innovative that doesn’t just stimulate an arms race and put all the power back into the hands of the fiat-wealthy. I don’t have a solution unfortunately, but hopefully someone will find one and bring about a new generation of digital currencies in the coming five to ten years. That being said, cryptocurrency as a space is very unpredictable so it wouldn’t surprise me at all if dogecoin beats the odds and overcomes these challenges in some weird, wacky way. It’s in the community’s hands, and they’re certainly passionate about seeing it reach the moon, as am I.”

Can this happen to bitcoin?

To be balanced, below is the network hashrate for the Bitcoin network following its first halvingday on November 28, 2012:

The following two months, from December 2012 through January 2013, the hashrate stayed flat and in some weeks even declined. There were three reasons why the network did not decline precipitously like dogecoin:

- Despite the fact that very little real commerce actually takes place on the bitcoin network, there was some amount that did in 2012 and does today (primarily gambling and illicit trading of wares). Thus there was external demand for the tokens beyond miners and tippers.

- The token prices rose creating appreciation expectations. The price rose from $12.35 on 28th November 2012 to $20.41 on 31st January 2012. If miners believe and expect the price to increase in value, they may be willing to operate at a short-term loss.

- The first batch of ASICs from Avalon shipped and arrived to their customers at the very end of January. These provided roughly two to four orders of magnitude per watt in performance than the top competing FPGAs and GPUs. This is equivalent of miners being given sticks of dynamite instead of pick axes to tunnel through mountains.

While more research will be conducted and published in the following months and years before the next bitcoin halvingday (estimated to occur probably before August 2016), the bitcoin network faces a similar existential hurdle, though perhaps less stark once more ASIC processes hit similar node fabrication limitations. That is to say, in the next couple of years there will no longer be performance gains measured in orders of magnitude. They will likely compete on energy costs. Since most participants do not like paying transaction fees, incentivizing miners to stay and provide security will likely be problematic for the same income reduction issues. This scenario will likely be revisited by many others in the coming months and years.

Nothing personal

From a marketing perspective Dogecoin has done more to bring fun and excitement to this sub-segment of digital currencies than most other efforts – remember, USD can also be digitized and encrypted. In turn it brought in a new diverse demographic base to block chain technology, namely women. While some of the more outlandish gimmicks will likely not be enough to on-ramp the necessary token demand which in turn leads to token appreciation, this project has not gone unnoticed.

For instance, two weeks ago I had coffee with a bank manager in the San Francisco financial district. As we were wrapping up he asked me to explain dogecoin. I mentioned that what sets doge apart from the rest was its community was much more open towards self-ridicule, self-parody, less elitist and most importantly, women actually attended meetups.

He quickly surmised, “Oh, so it’s the wingman currency. It’s the friend you bring to the bar who is willing to look goofy to help you out.”

That is probably a fair enough assessment and it will likely need a wingman to survive.

Open your free digital wallet here to store your cryptocurrencies in a safe place.

What are Bitcoin nodes and why do we need them?

peer-to-peer (P2P) network. However, what’s often lost in translation is

the sheer amount of machinery that is needed to maintain this global

infrastructure.

transactions, bitcoin requires more than a network of miners processing

transactions, it must broadcast messages across a network using ‘nodes’.

This is the first step in the transaction process that results in a

block confirmation.

network must not only provide an avenue for transactions, but also

remain secure. By using a number of randomly selected nodes, the network

can reduce the problem of double spending – when a user attempts to spend the same digital token twice.

bitcoin doesn’t just need nodes, it requires lots of fully functioning

nodes – nodes that have the bitcoin core client on a machine instance

with the complete block chain. The more nodes there are, the more secure

the network is.

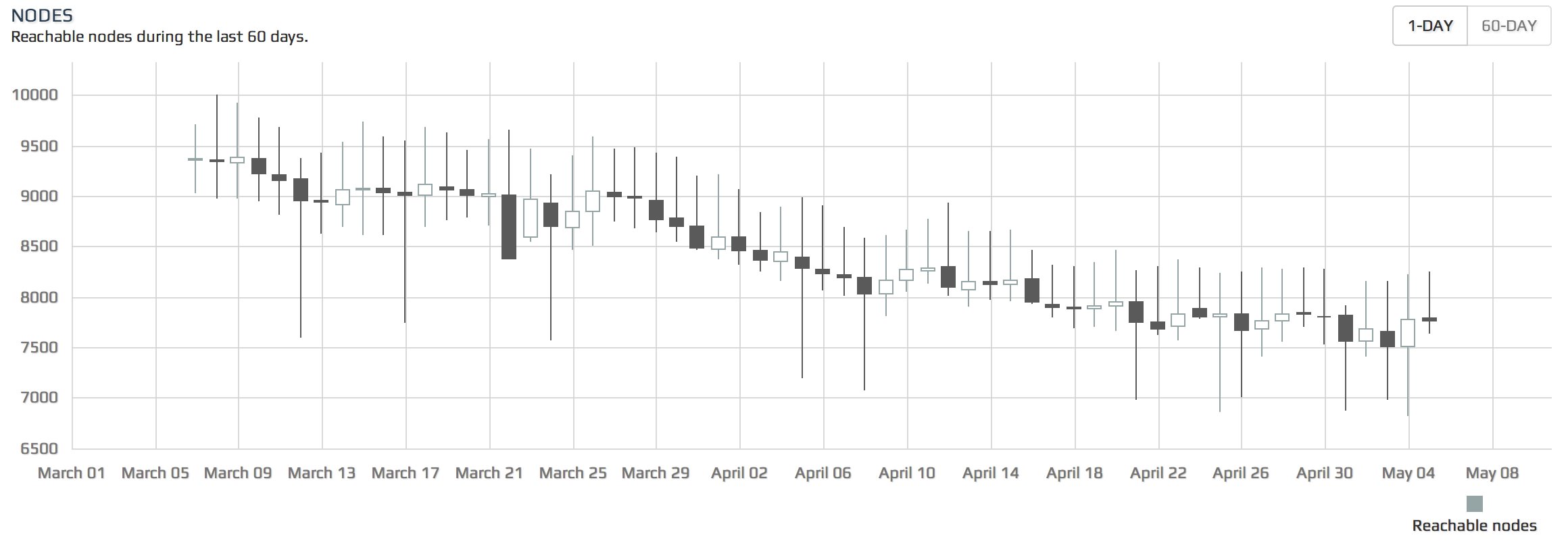

Waning support

at a 60-day chart of bitcoin nodes shows that the number has gone down

significantly. It went from 10,000 reachable nodes in early March to

below 8,000 at the beginning of May.

|

|

Source: Bitnodes |

interesting is that during a recent 24-hour period, the number of

reachable nodes went down from 8,200 to 7,600 and back to 8,200 again.

This suggests that a portion of users running nodes are turning off

their machines at night, meaning that this contingent of nodes are being

run on desktops or laptops.

|

|

Source: Bitnodes |

|

|

A map based on Bitnodes data. Source: Coinviz |

Lack of incentive

running a bitcoin node does not provide any incentive. The only benefit

for someone to run a node is to help protect the network, and based on

the Bitnodes data, the number of people interested in supporting the

network with a full node is waning.

Centralization of mining

terms of supporting the bitcoin network, it used to be a lot easier for

the average user to participate. However, the advent of massive ASIC

data centres has weakened the consensual nature of mining, and by

extension providing nodes, for many people.

“As

bitcoin grows, so does the network and the computing power behind the

scenes required to run it. The majority of bitcoiners won’t be able to

support their own nodes and will be taken over by companies like KnC.”

pushing bitcoin towards a more centralized future. McKelvie also

believes that major technology companies that take interest in bitcoin

will have to put their computing resources behind the digital currency:

“I

wouldn’t be surprised if we see large tech companies like Google and

Amazon throwing resources at bitcoin as they adopt the currency.”

Feedback from nodes

sees the issue of nodes dropping from 10,000 down to under 7,000 as a

significant problem. To Hearn, the core of the issue is disinterest in

both expending computing resources and electricity toward something that

may have diminishing value.

Hearn has proposed added functionality that would allow communications

between nodes and the developers to better understand why so many are

dropping out.

is because their number will continue to decline no matter what – and

they appear to only be working when users are awake during the day.

“It

makes [the bitcoin network] ‘seem’ bigger, more robust and more

decentralised, because there are more people uniting to run it. So

there’s a psychological benefit.”

Moving forward

believes that community attention to the lack of nodes supporting the

network is what the industry needs in order to boost numbers:

“I agree we need more full nodes. I’ve long been a proponent of such calls for more nodes.”

such calls for voluntary support might not be enough motivation for

people to do so, though, so, one logical idea that has been floated is

to give nodes some sort of incentive.

feasible right now: over the past six months, miners have been

averaging a daily reward of 15.98 BTC per day, according to Blockchain.

bitcoin prices would peg that value at around $7,040 per day for the

entire network – and the growth in transaction fees has been incredibly

flat over the past six months. As a result, miners would likely be

reluctant to concede any revenue to bitcoin nodes, which don’t require

pricey ASIC hardware to run.

|

|

Transaction fees on the network for past six months. Source: Blockchain |

of the bitcoin community seem to be losing interest in hosting full

nodes. And it’s something to pay attention to, because over time it

might mean that the major companies in the industry may have to pick up

the slack.

the network as full nodes, though, it continues to lessen the amount of

decentralization the network has at an infrastructure level.

is all down to circumstances surrounding bitcoin sentiment – the rise of

ASICs, the selloffs in China and complete collapse of Mt. Gox – plus

little in the way of incentives for someone to run a node.

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Marc Andreessen: In 20 years, we’ll talk about Bitcoin like we talk about the Internet today

(WashingtonPost) The investor and Web browser pioneer Marc Andreessen thinks we’ll

all look back in 20 years and conclude that Bitcoin was as influential a

platform for innovation as the Internet itself was. He says that tech

companies think their meetings with President Obama on privacy are a

waste of time. And he calls net neutrality a “lose-lose.” In a

wide-ranging interview with The Washington Post this week, Andreessen

painted a picture of a future that’s distributed, messy and fraught

with tension. Here’s an edited transcript of our conversation.

Is there anything that Washington has built a wall against in terms of progress?

Well, the big thing right now for the tech industry is the Snowden

revelations, and the consequences of that for the American tech

industry. Specifically, in two areas: One is that the level of trust

that customers have [in] American tech companies has been seriously

damaged. And that is especially — but not exclusively — true outside the

United States. Every time another revelation comes out, like the one

this weekend about hijacking the routers on their way out of the country, or the one about hacking into the Internet companies’ backbone networks — every time one of these shoes drops, and apparently there is just an unlimited

number of shoes — every time one of these things happens, it’s a

serious blow to the credibility of these companies, especially outside

the U.S. And so there’s a really big, I mean very, very, very high level

of concern in the Valley that the American tech industry is in trouble

outside the U.S.

And then, two is this balkanization of the Internet that’s happening

now. As more revelations happen, more and more countries are saying:

“Okay, if we can’t trust the Internet, if the NSA is going to watch

everybody on the Internet all the time, we’re going to have to break off

and have our own Internet. Have our own firewalls, do what the Chinese

do, have our own private Internet or whatever the hell it’s going to

be.” This issue is being used as political cover for what these countries want to do anyway.

That brings us to, “Okay, how is the American government getting in

front of this?” And the answer is, “Not even a little bit.” The view in

the Valley is that the White House has hung the NSA out to dry. Just

like, “You’re on your own.” And there’s basically no effective

communication right now that I’m aware of between the American

government, especially the administration and American tech companies,

on like, “Okay, what happens now?”

There isn’t?

No.

Those meetings that occurred, that’s just for show?

Yeah, people come back, and they’re like, “Nothing happened.” The

Obama administration does not seem to have any real — they don’t seem to

have a plan. They seem to be in the mode of they kinda hope that it

goes away. And they hope that if they get face time with the execs they

can just mollify everybody and over time, the issue will just dissipate.

But I’m not aware of any substance that’s come out of those meetings.

I’m not aware of anybody who’s come back from those meetings saying:

“Okay, now there’s a plan. Now we know what’s going to happen.” It’s

been the opposite. It’s been people saying, “I don’t even know why I

went.”

Is there anything tech companies can do, whether on the Snowden stuff, or culturally?

These technologies escalate the power of government, but they also

escalate the power of business, and they also escalate the power of

individuals. So everyone’s been upgraded. And it’s a recalibration of

who can do what, and everybody can do new things, so everybody’s uneasy

about it. Governments are very worried about what citizens are going to

be able to do with these new technologies. Citizens are very worried

about what governments are going to do, and everybody’s worried about

what businesses are going to do. It’s this three-way dynamic that’s

playing out. And so for any of these individual issues, it’s not just

“What is one leg of this triangle going to be doing?” It’s, “What are all three of them going to be doing, and how will the tension resolve itself?”

Any thoughts on all these mergers that are being announced?

Not specifically on the mergers.

Or net neutrality?

So, I think the net neutrality issue is very difficult. I think it’s a

lose-lose. It’s a good idea in theory because it basically appeals to

this very powerful idea of permissionless innovation. But at the same

time, I think that a pure net neutrality view is difficult to sustain if

you also want to have continued investment in broadband networks. If

you’re a large telco right now, you spend on the order of $20 billion a

year on capex. You need to know how you’re going to get a return on that

investment. If you have these pure net neutrality rules where you can

never charge a company like Netflix anything, you’re not ever going to

get a return on continued network investment — which means you’ll stop

investing in the network. And I would not want to be sitting here 10 or

20 years from now with the same broadband speeds we’re getting today. So

the challenge, I think, is to accommodate both of those goals, which is

a very difficult thing to do. And I don’t envy the FCC and the

complexity of what they’re trying to do.

The ultimate answer would be if you had three or four or five

broadband providers to every house. And I think you actually have the

potential for that depending on how things play out from here. You’ve

got the cable companies; you’ve got the telcos. Google Fiber is

expanding very fast, and I think it’s going to be a very serious

nationwide and maybe ultimately worldwide effort. I think that’s going

to be a much bigger scale in five years.

So, you can imagine a world in which there are five competitors to

every home for broadband: telcos, cable, Google Fiber, mobile carriers

and unlicensed spectrum. In that world, net neutrality is a much less

central issue, because if you’ve got competition, if one of your

providers started to screw with you, you’d just switch to another one of

your providers.

There’s more and more integration between Bitcoin and the

financial services sector. But a lot of people who support Bitcoin

supported it because it was sort of disconnected from the infrastructure represented by government and everything else.

So we sort of have a theory on this, on where really disruptive

technologies come from. So the really new disruptive technologies come

from the fringe. This was true of PCs. Steve Jobs was, like, a

hippie. Internet came from the fringe. No big technology company thought

the Internet was going to be important, right up until basically 1995

or 1996.

Bitcoin is the classic instance of that. Bitcoin didn’t come from

Citibank; it didn’t come from the Federal Reserve; it didn’t come from

Visa. It came from the fringe. And now Bitcoin is in the early stages of

mainstreaming today. And the signs that it’s in the early stages of

mainstreaming are mainstream venture capital firms funding mainstream

startups, employing mainstream engineers to build services that’ll be

used by mainstream people. You’ve got big companies that are not yet

doing a lot with it, but are looking very seriously at it. So every big

bank has people that are trying to figure out what to do with Bitcoin;

every big e-commerce company has people that are trying to figure out

Bitcoin. You have mainstream regulators figuring it out; you’ve got

people at the Federal Reserve, and the Treasury Department and IRS that

are figuring it out. At the state level, people are engaged on it. And

so, it’s in the early stages of mainstreaming.

It’s already happening.

Anybody who thinks Bitcoin makes it easier to do transactions that aren’t

tracked by the government is 100 percent wrong. The transactions all

happen in public view. Anybody can look at the entire ledger and verify

who owns what. So if you’re a law enforcement agency or an intelligence

agency, this is a much easier way to track the flow of money than cash.

So I think actually law enforcement and intelligence agencies are going

to wind up being pro-Bitcoin, and libertarians are going to wind up

being anti-Bitcoin.

For [journalists], the big challenge has been explaining what

Bitcoin is to people. And I think we’ve always explained it as a

currency, but does that — now that people know about it in terms of a

currency, does that prevent them from [grasping Bitcoin’s full

potential]?

I have a lot of friends who are programmers. The programmers have always gone like, “Those [Bitcoin] guys are crazy.”

And then, almost 100 percent of the time, they sit down, read the paper,

read the code — it takes them a couple weeks — and they come out the

other side. And they’re like: “Oh my god, this is it. This is the big

breakthrough. This is the thing we’ve been waiting for. He solved all

the problems. Whoever he is should get the Nobel prize — he’s a genius.

This is the thing! This is the distributed trust network that the

Internet always needed and never had.”

So, one of the challenges is you take people who aren’t

professional programmers or mathematicians and then you expect them to

understand it from a standing start. And it’s daunting. And so then it

gets a word attached to it, like “currency” or whatever you want to call

it, and then people think that it is something it isn’t. And you have a

sense of this, but it’s a much deeper concept than currency. It’s the

idea of distributed trust.

So the business opportunity posed by this “distributed trust

network” — as an investor, what do you see that you could potentially —

Hundreds or thousands of applications and companies that could get built on top.

Is this, like, a billions-of-dollars kind of industry?

Yeah.

Trillions…?

Yeah! (Laughs, steeples his fingers Mr. Burns-style). Yeeeah… (Laughs) I have the haircut, I can do it.

Digital stocks. Digital equities. Digital fundraising for companies.

Digital bonds. Digital contracts, digital keys, digital title, who owns

what — digital title to your house, to your car. Like for example, you

get a digital title on a car, attached to a digital key, where you own

your car on the Bitcoin blockchain and on your smartphone. The key for

opening your car and starting your car is tied to that title. And if I

sell you my car, automatically you get title, and you get the key that

lets you operate the car, and it’s all digital, and it’s all unique, and

it can’t be cracked. You’ve got digital voting, digital contracts,

digital signatures. You’ve got unique pieces of digital content. If you

guys wanted to know exactly who had every piece of content you ever

made, you can track that. It’s this long list. And then every aspect of

financial services: insurance contracts, insurance derivatives, currency

exchange, remittance — on and on and on. It gives you a chance to

basically go after this very broad category of online business in a new

way. And, by the way, if we had had this technology 20 years ago, we

would’ve built it into the browser.

E-commerce would’ve gotten built on top of this, instead of getting

built on top of the credit card network. We knew we were missing this;

we just didn’t know what it was. There is no reason on earth for anybody

to be on the Internet today to be typing in a credit card number to buy

something. It’s insane, because — which is why you have all these

security problems, the Target hack and all this crazy…. And these high

fees, this high fraud rate. It doesn’t make sense online to have a

payment mechanism that requires you to hand over your credentials to

make a payment. That’s just an invitation to fraud and identity theft.

It’s just stupid.

But we didn’t have the better way of doing it. So we didn’t know what

else to do, and now we have the better way of doing it. Now, it’s going

to take time. We’re quite confident that when we’re sitting here in 20

years, we’ll be talking about Bitcoin the way we talk about the Internet

today. We just need time for it to play out.

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Bitcoin used to buy $500,000 Kansas home

they knew it was pretty cool,” he said. “This seemed like a good test of

how far the currency has come.”

|

| When Josh Zerlan went looking for a new home, he originally didn’t think about using a bitcoin to buy it. |

banks take their cut. They take a fee, you end up paying quite a bit of

money. With bitcoin, you don’t have to pay any of those fees, and it is

an instant transfer,” he said.

with his knowledge of it, so we took the plunge,” Tim Hoelting said.

bitcoins, although more than 30,000 businesses currently take them

online.

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Federal reserve advisory council sheds positive light on Bitcoin

In February, much of the community rejoiced when Federal Reserve Chairwoman Janet Yellen insisted that the regulatory entity had no authority to when it came to the digital currency.

A recently obtained document from a Federal Reserve Advisory Committee meeting early this month has shed some light on this very topic, in return, revealing exactly how the Fed plans on reacting to the relatively new and emerging technology.

The Federal Advisory Council and Board of Governor’s record of meeting devoted a special section of the outline to bitcoin specifically. Among the key topics of concerns listed in respect to the digital currency were whether or not bitcoin has the potential to cause the “disruption of traditional channels of commerce with high potential for illicit use.” In respect to banking, the document also questions the possible “disintermediation of traditional payment networks, promoting shadow transacting.”

In the eyes of the Fed, indications point that the outlook is unanimous in that rather than posing as threat, bitcoin, with increased regulation, may hold promise:

Bitcoin does not present a threat to economic activity by disrupting traditional channels of commerce; rather, it could serve as a boon … Its global transmissibility opens new markets to merchants and service providers … Driving capital flows from the developed to the developing world should increase consumption.

The Federal Advisory Council (FAC) is comprised of twelve elite representatives of the banking industry. The committee meets four times a year, as required, to consult with and advise the Board on all matters within the Board’s jurisdiction. The overall rhetoric among the committee is that the board echoes the voice of Silbert in that the current financial institutions will play a key role in bitcoin’s future. The FAC ‘s conclusion was that, “should [bitcoin] adoption accelerate, banking could participate increasingly in bitcoin fund flows, especially as multicurrency accounts proliferate and reputational concerns subside.”

The FAC’s stance on bitcoin supports a reversal in the plethora of bad news encompassing the digital currency. Following easing tensions in China, the wildly successful Bitcoin2014 conference in Amsterdam, which delivered a surplus of positive news along with several major announcements, bitcoin has surged in value over that past several hours. Prices on Bitstamp rose from an opening of $448.34, while spiking as high as $500.00 mid-day as optimism surrounding the digital currency continues to influence bitcoin’s value.

Open your free digital wallet here to store your cryptocurrencies in a safe place.

‘Cryptocurrency’ officially added to Oxford dictionary online

‘cryptocurrency’ to its database. The decision was made as part of a

quarterly update this May that also included the words ‘bikeable’,

‘snacky’ and ‘time suck’.

“A

digital currency in which encryption techniques are used to regulate

the generation of units of currency and verify the transfer of funds,

operating independently of a central bank.”

Usage examples

ODO further provided example sentences that, in part, aim to sum up the

values of those who are interested in the industry and community.

“Decentralized

cryptocurrencies such as bitcoin now provide an outlet for personal

wealth that is beyond restriction and confiscation.”

sentences describe how cryptocurrencies are valued based on supply and

demand, and highlight that the total value of the market is more than

$8bn.

Contemporary language

noted by Angus Stevenson, Head of Dictionary Projects at Oxford

University Press in a 2013 interview with CoinDesk, inclusion in the ODO

“doesn’t make any judgement on whether [the word] is good, bad,

worthwhile or anything else”.

Dictionary is more of a historical cannon that includes words and

definitions that have stood the test of time.

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Winklevoss twins betting Bitcoin will be bigger than Facebook

(NewsBTC) The duo — who infamously won a multimillion dollar settlement from

Facebook following claims Mark Zuckerberg had ripped off their idea —

says that bitcoin could very well become bigger than Facebook, says The Guardian.

|

| The Winklevoss twins are betting big on bitcoin. |

Facebook, of course, is the world’s largest social network — with a user base exceeding one billion.

The two came to learn about bitcoin whilst on holiday in Ibiza, saying they were “fascinated from day one.”

And while bitcoin’s $5.67 billion market cap doesn’t come close to

touching Facebook’s $150 billion cap, the Winklevosses put their faith

in the digital currency for the reason that it has more potential to be

more impactful than a social network.

“Bitcoin potentially could be more impactful because being able to

donate 50 cents to someone across the world has more impact than

potentially sharing a picture,” said Tyler Winklevoss.

“But they’re very different. Facebook is like the internet – a large

company and an application. Bitcoin is a protocol for decentralisation,

so you could build a decentralised company on top of it, a stock market.

It’s an internet of ownership, so it’s not quite a direct comparison.”

For critics who point to bitcoin’s volatility as a reason it can

never be widely successful, the twins say that’s basically a

non-statement.

“Unregulated assets with unclear regulatory landscapes are always

going to be volatile. That’s what unregulated assets do,” said Tyler,

who points to the early days of the Internet as an example of a

technology that can go from an enthusiast’s interest to a worldwide

phenomenon.

The twins, who are working on the own bitcoin ETF (and also recently launched a price index) predict that this is the year Wall Street becomes heavily involved in the bitcoin-o-sphere.

Already, we’re seeing incredibly amounts of investor interest,

especially in the wake of two major price spikes that eventually brought

the price of bitcoin above $1,000 late last year.

The Winklevosses are estimated to own one percent of bitcoins presently in circulation.

Open your free digital wallet here to store your cryptocurrencies in a safe place.

NXT: Bitcoin rival or ally?

(BitScan) NXT is a relative newcomer to the cryptocurrency scene but in the six months since it was launched it has steadily risen in value and profile, now claiming the fifth spot on the Coin Market Cap table.

At the time of writing, NXT has just surpassed Dogecoin with a market cap comfortably over $30 million.

NXT’s Asset Exchange allows direct P2P trading of digital assets

an innovative new platform unveiled on Monday that enables direct P2P

trading of digital assets. The idea is simple but striking. The Asset

Exchange does for shares in companies and other digital assets what

bitcoin (and other cryptocurrencies, including NXT) do for cash. It’s

not the first entrant to the market, for sure; bitshares.org,

for example, is the NXT Asset Exchange’s direct competitor and was

already up and running before the AE launched. But NXT’s client is an

elegantly simple, easy-to-use platform, and the Exchange functionality

is integrated into the cryptocurrency from the ground up. To look at it

another way, NXT was conceived as the foundations of a digital economy,

whereas bitcoin was originally conceived as, primarily and

predominantly, a currency. Their relative timing and positioning give

them each unique advantages and disadvantages.

NXT vs Bitcoin

‘the next bitcoin’, the rival that will unseat the father and

grandfather of all altcoins. All of these claims have to be taken with

at least a pinch of salt, and very often a truckload. The reality is

that bitcoin is armoured from any such attack by a very powerful force: the network effect.

Put simply, this means that the sheer number of people using and

invested in bitcoin alone makes it very difficult for any contender to

unseat it. The more people join a network – be that a telephone network,

a social network or a currency network such as bitcoin – the more

useful it becomes and so the more it cements its own position. Thus

whatever the pros and cons of bitcoin vs other cryptocurrencies,

whatever advantages they offer in theory, it is extremely unlikely that bitcoin will lose its top spot any time soon.

NXT is built along different lines to bitcoin, both ideologically and

NXT is built along different lines to bitcoin, both ideologically andpractically. It uses a proof-of-stake system and ‘forging’ rather than

bitcoin’s proof-of-work mining system, for example – something that has

drawn both admiration and controversy. This has various implications for

anything from coin distribution to power consumption and the hardware

needed to participate in the network. Unsurprisingly, dyed-in-the-wool

bitcoin-lovers have expressed doubt about some of NXT’s flagship

features; unsurprisingly, some of NXT’s cheerleaders see these same

features as killer advantages.

bitcoin. In fact, NXT offers features that can and likely will boost

bitcoin’s adoption, as well leveraging bitcoin’s popularity to improve

its own reach.

Ultimately, the world is a big

place and cryptocurrency hasn’t yet been taken up by more than a

fraction of one percent of the population. Like any other area of life,

cryptocurrency enthusiasts have a tendency to be tribalistic. At this

point, though, the real competition isn’t between bitcoin and other

cryptocurrencies. It’s between cryptocurrency and fiat systems. If one

cryptocurrency offers another a leg up and thereby increases the

adoption of both, that’s good for everyone.

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Top 5 businesses that accept Litecoin payments

(CoinReport) Litecoin is the second most valued digital currency on the market, only being bested by bitcoin. However, litecoin is not just a knock-off to the world’s first digital coin. It was intended by its developers to improve on the structure set forth by bitcoin.

The main two differences that separates litecoin from bitcoin:

1) Litecoin processes a block every two and a half minutes, while bitcoin processes a block every 10 minutes.

2) Litecoin will total 84 million coins, unlike bitcoin’s cap of 21 million.

The digital currency continues to catch individuals and business owners by storm, as more businesses are accepting it as a form of payment. CoinReport has compiled a list of the Top 5 businesses that have begun implementing Litecoin into their finances.

Top 5 businesses that welcome Litecoin payments

5. Ellenet

“Crypto currencies are the future, it’s plainly obvious and people need to understand that Bitcoin and other coins are not going away. Without sounding terse, you can’t stop progress.”

digital payments, it hopes to grow even larger. In addition, Ellenet works with digital mining company Petabit Pty. Ltd,

who works on mining both litecoins and bitcoins. The partnership with Petabit will allow Ellenet to get into more digital currency-based ventures.

4. Sean’s Outpost

3. eGifter

2. KnCMiner

“You will find the Litecoin payment method option when you complete an order through the checkout on our website.”

1. Benz and Beamer

“GoCoin makes it extremely easy for us to accommodate new customers looking to

pay with bitcoin and other emerging digital currencies like litecoin.

Their platform secures the coin exchange for cash within minutes,

creating a real win/win for my dealership and my customers.”

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Give $250,000 in Bitcoin, get second citizenship

with a Las Vegas escort.

Bitcoin these days.

that sets clients up with citizenship to balmy Caribbean island-nation St.

Kitts and Nevis, payable in cryptocurrency. St. Kitts and Nevis has offered a

‘citizenship by investment’ program since 1984 that accepts investment into the

local economy in exchange for a spanking-new passport.

isn’t cheap. Wannabe citizens must either buy local real estate worth $400,000

or more, or donate at least $250,000 to the Sugar Industry Diversification

Foundation (SIDF) – on top of a nonrefundable application fee of about $60,000

per applicant plus an additional $30,000 for each one of his or her dependents.

holding a St. Kitts passport offers a number of benefits. Aside from the

stunning seas, sands, and climate offered by the Caribbean country, St. Kitts doesn’t

take any income, wealth, or inheritance taxes; citizens get visa-free travel to

140 countries and a 10-year multiple-entry visa to the United States.

countries or ones with invasive policies on individual privacy, the citizenship

process offers more abstract benefits: freedom and privacy.

stories from around the globe about upheaval, increased taxes, and governments

exerting more and more control over citizens’ freedoms and privacy,” the

Passports for Bitcoin website says. “Having a second citizenship and passport

in a stable country is now a must in order to hedge against governmental

intrusion and excessive taxation.”

home countries aren’t notified that their citizens have applied for or received

a second citizenship.

Kitts passport with Bitcoin isn’t clear. The website of the project’s parent company,

International Investments & Consulting, Ltd., says it has processed over

100 applications, though it does not specify how they were paid for.

popular amongst the rich and famous. Roger Ver, an American Bitcoin

entrepreneur and ‘angel investor’ in Bitcoin startups, has bought himself a

passport to St. Kitts, as has as the so-called “Most

Interesting Man on Instagram” millionaire/poker player/playboy Dan

Bilzerian.

ago as a hedge against possible world political turmoil which could negatively

affect the United States,” Bilzerian wrote in a testimonial

on the Passports for Bitcoin website. “I value freedom more than almost

anything else and a second or third passport provides me insurance just in case

the U.S. government decides to value security over freedom.”

St. Kitts citizenship last month after fleeing the country under pressure from

the government over data protection and privacy.

passport in Bitcoin.

Open your free digital wallet here to store your cryptocurrencies in a safe place.