15 May

0

How we know Bitcoin is not a bubble

The Value of Money

(NakamotoInstitute) No matter how many times Bitcoin grows by orders of magnitude,

holdouts still remain who argue that it is a bubble destined to fail. To

address this claim, I will describe a theory that describes how to

appraise Bitcoin according to the Austrian theory of money.

holdouts still remain who argue that it is a bubble destined to fail. To

address this claim, I will describe a theory that describes how to

appraise Bitcoin according to the Austrian theory of money.

In Austrian economics, money is valuable because it is liquid. This

means that a given value of money is demanded everywhere and can easily

be traded for goods. For example, say I had enough bitcoins to buy a

100-oz gold bar. In late 2010, this would have been worth around one to

two million bitcoins and would have been impossible to sell on the open

market without drastically affecting the price. By contrast, in early

2014, 100 ounces of gold was worth about 100 bitcoins, and this amount

could easily have been traded quickly on one of the major exchanges

without affecting the price noticeably. Thus, in early 2014 Bitcoin was

more liquid than in late 2010, and was therefore a better currency.

means that a given value of money is demanded everywhere and can easily

be traded for goods. For example, say I had enough bitcoins to buy a

100-oz gold bar. In late 2010, this would have been worth around one to

two million bitcoins and would have been impossible to sell on the open

market without drastically affecting the price. By contrast, in early

2014, 100 ounces of gold was worth about 100 bitcoins, and this amount

could easily have been traded quickly on one of the major exchanges

without affecting the price noticeably. Thus, in early 2014 Bitcoin was

more liquid than in late 2010, and was therefore a better currency.

Unfortunately, this insight about the value of money does not give us

a means of appraising it because the liquidity cannot be separated from

the price. This is kind of a problem—it sounds like a circular argument

because it says that Bitcoin’s value is caused by its price! This

allows for no way to detect whether Bitcoin is overvalued or

undervalued.

a means of appraising it because the liquidity cannot be separated from

the price. This is kind of a problem—it sounds like a circular argument

because it says that Bitcoin’s value is caused by its price! This

allows for no way to detect whether Bitcoin is overvalued or

undervalued.

In order to prevent this model from being causally circular, a time

element is required. Our observations about money come from the past,

whereas our judgments about its value are about the immediate future.

This makes the value of money into a positive feedback loop. If the

network is growing, then it will tend to continue to grow, whereas if it

is shrinking, it will tend to continue to shrink.

element is required. Our observations about money come from the past,

whereas our judgments about its value are about the immediate future.

This makes the value of money into a positive feedback loop. If the

network is growing, then it will tend to continue to grow, whereas if it

is shrinking, it will tend to continue to shrink.

This model of money has no independent quantity that estimates

anything like an underlying value. Any price is as good as any other—the

only thing that matters is the direction it is moving. This is not

really an appraisal after all—but it is still the right way to

understand Bitcoin’s price.

anything like an underlying value. Any price is as good as any other—the

only thing that matters is the direction it is moving. This is not

really an appraisal after all—but it is still the right way to

understand Bitcoin’s price.

Bubbles

In the short term, there is money to be made by buying anything whose

price is showing an upward trend if one spots the trend early enough.

In other words, if one can predict that other people are likely to

appraise a good more highly in the future, regardless of whether that

appraisal is rational or irrational, then it makes sense to buy into the

change of sentiment. If lots of people begin to think this way, then

they can create a positive feedback among one another and bid up the

good beyond any rational appraisal of it. This is a bubble.

price is showing an upward trend if one spots the trend early enough.

In other words, if one can predict that other people are likely to

appraise a good more highly in the future, regardless of whether that

appraisal is rational or irrational, then it makes sense to buy into the

change of sentiment. If lots of people begin to think this way, then

they can create a positive feedback among one another and bid up the

good beyond any rational appraisal of it. This is a bubble.

A bubble bursts because eventually people have to get around to using

a good for its ultimate purpose. Once it is understood that the people

who actually use the good are being bid out of the market, then the

price crashes because people stop predicting higher and higher

appraisals to the price.

a good for its ultimate purpose. Once it is understood that the people

who actually use the good are being bid out of the market, then the

price crashes because people stop predicting higher and higher

appraisals to the price.

Money, however, need not have any ultimate use. It may only ever

passed around from person to person, without ever being consumed. A

stock is valued by the sum of its interest-adjusted dividends. A bond is

valued by its redemption value adjusted by the interest rate and the

risk of default. A commodity is valued by the value of the goods it can

be used to produce. However, for money, there is no independent quantity

to provide a reality check. All money is like a bubble that never

bursts.

passed around from person to person, without ever being consumed. A

stock is valued by the sum of its interest-adjusted dividends. A bond is

valued by its redemption value adjusted by the interest rate and the

risk of default. A commodity is valued by the value of the goods it can

be used to produce. However, for money, there is no independent quantity

to provide a reality check. All money is like a bubble that never

bursts.

Metcalfe’s Law

Some of the theory of money can be understood in terms of Metcalfe’s law

from computer networking. Metcalfe’s law says that the value of a

network is proportional to the square of the number of nodes. The

rationale is that the network should be valued according to the number

of connections it supports, which is approximately proportional to n2 (for large n).

Consequently, as the network grows, it presents a better and better

opportunity for new members. As new members enter, the network improves

for all its present members.

from computer networking. Metcalfe’s law says that the value of a

network is proportional to the square of the number of nodes. The

rationale is that the network should be valued according to the number

of connections it supports, which is approximately proportional to n2 (for large n).

Consequently, as the network grows, it presents a better and better

opportunity for new members. As new members enter, the network improves

for all its present members.

Metcalfe’s law must be adjusted slightly to apply to media of

exchange because some nodes in the trade network will be more valuable

than others. Those who have a lot of the medium are potentially able to

spend more than those who have little. Therefore, use the market cap of

the medium of exchange as n instead of the number of people.

Similarly, some transactions are also worth more than others, so it

makes sense to use the transaction volume rather than the number of

transactions.

exchange because some nodes in the trade network will be more valuable

than others. Those who have a lot of the medium are potentially able to

spend more than those who have little. Therefore, use the market cap of

the medium of exchange as n instead of the number of people.

Similarly, some transactions are also worth more than others, so it

makes sense to use the transaction volume rather than the number of

transactions.

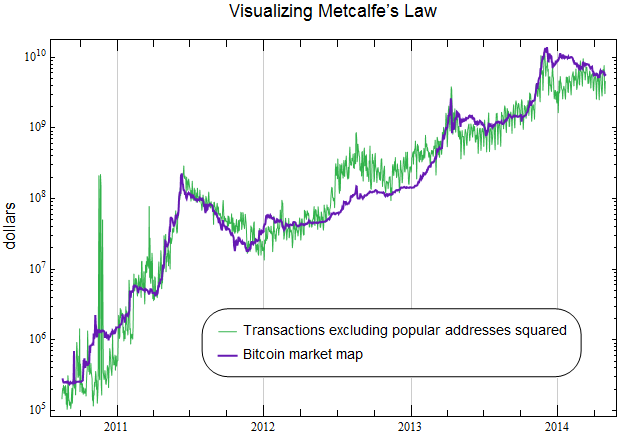

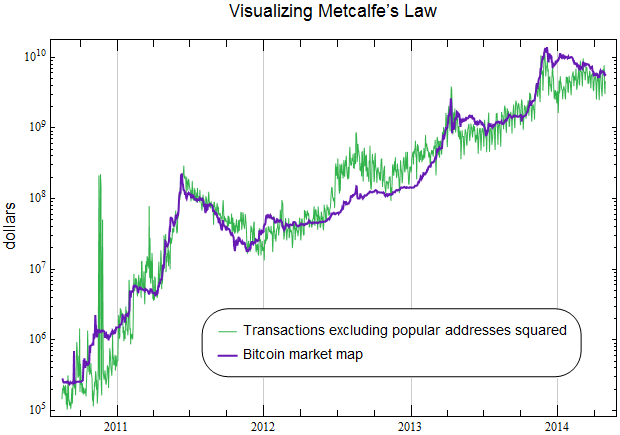

A striking test of Metcalfe’s law in Bitcoin recently appeared on the Bitcointalk forums, created by Peter R. I have made my own chart here.

This chart plots the market cap in blue and the square of the

transaction volume excluding popular addresses in green. The axis on the

is the price in dollars. Exactly as Metcalfe’s law predicts, the

transaction volume increases very neatly as the square root of the size

of the network. The correspondence is beautiful. I wish I had thought to

make it first!

transaction volume excluding popular addresses in green. The axis on the

is the price in dollars. Exactly as Metcalfe’s law predicts, the

transaction volume increases very neatly as the square root of the size

of the network. The correspondence is beautiful. I wish I had thought to

make it first!

I would like, however, to criticize the interpretation of the

diagram. On the original Bitcoin Talk, thread, the green plot has been

labeled as the “Metcalfe Value”, as if it is an appraisal of the Bitcoin

that estimates what it could cost.

diagram. On the original Bitcoin Talk, thread, the green plot has been

labeled as the “Metcalfe Value”, as if it is an appraisal of the Bitcoin

that estimates what it could cost.

This interpretation is incompatible with the theory of the value of

money I presented above. In my theory, the value causes the

transactions, whereas in the diagram, the transactions cause the value.

However, it is only potential transactions that cause the value. Past

transactions are of no value to anybody. The present size of the

network and the consequent opportunities is likely to provide tomorrow

will motivate people to buy and sell today.

money I presented above. In my theory, the value causes the

transactions, whereas in the diagram, the transactions cause the value.

However, it is only potential transactions that cause the value. Past

transactions are of no value to anybody. The present size of the

network and the consequent opportunities is likely to provide tomorrow

will motivate people to buy and sell today.

This may seem like hair-splitting, but a confusion of cause and

effect can have serious consequences. For example, many people believe

that it is necessary to spend bitcoins and increase the transaction

volume in order to make Bitcoin more valuable. Of course this is

nonsense; all this does is fill up the network with transactions for

things that nobody actually wanted. That does not present a good value

for a newcomer because he will want a network that presents him with real

opportunities, not just ways of artificially increasing transaction

volume. The more that the Bitcoin network is focused on artificially

increasing the transaction volume to make it look good, the more it

resembles a Ponzi scheme. Rather, to make the network more valuable, we should be hoarders. This is more likely to present newcomers with lots of potential uses for Bitcoin as a medium of exchange.

effect can have serious consequences. For example, many people believe

that it is necessary to spend bitcoins and increase the transaction

volume in order to make Bitcoin more valuable. Of course this is

nonsense; all this does is fill up the network with transactions for

things that nobody actually wanted. That does not present a good value

for a newcomer because he will want a network that presents him with real

opportunities, not just ways of artificially increasing transaction

volume. The more that the Bitcoin network is focused on artificially

increasing the transaction volume to make it look good, the more it

resembles a Ponzi scheme. Rather, to make the network more valuable, we should be hoarders. This is more likely to present newcomers with lots of potential uses for Bitcoin as a medium of exchange.

Appraising Bitcoin

A real good, of course, can have value due to a network effect and some productive use. Gold, for example, can be money and used as components in electronics. If there were ever a time when gold were used only

for electronics, but were then to acquire use as money once a network

effect formed around their price, an investor might be excused to call

the price an unsustainable bubble. However, it would turn out to be a sustainable bubble that inflates until it fills the entire economy. At least until Bitcoin came along.

for electronics, but were then to acquire use as money once a network

effect formed around their price, an investor might be excused to call

the price an unsustainable bubble. However, it would turn out to be a sustainable bubble that inflates until it fills the entire economy. At least until Bitcoin came along.

This brings us to Bitcoin. To what extent is Bitcoin’s price a

rational appraisal or an investment bubble? The answer is easy, much

easier than with a commodity like gold. Bitcoins have almost no use

other than as a medium of exchange. Thus, the fact Bitcoin has any

price at all is evidence that there is a real network effect. It is

much easier to prove that Bitcoin acts like money than that gold does,

in fact.

rational appraisal or an investment bubble? The answer is easy, much

easier than with a commodity like gold. Bitcoins have almost no use

other than as a medium of exchange. Thus, the fact Bitcoin has any

price at all is evidence that there is a real network effect. It is

much easier to prove that Bitcoin acts like money than that gold does,

in fact.

Each step in Bitcoin’s growth follows the same pattern. Any demand

for Bitcoin at all is enough to make it function as a medium of

exchange. If demand continues to grow, then it becomes a better medium

of exchange. There is no end to this process because the primary value

of Bitcoin is the network effect surrounding it, not any final

productive use.

for Bitcoin at all is enough to make it function as a medium of

exchange. If demand continues to grow, then it becomes a better medium

of exchange. There is no end to this process because the primary value

of Bitcoin is the network effect surrounding it, not any final

productive use.

Thus, Bitcoin is not a bubble. Its growth is like a self-fulfilling

prophesy: as more people believe in it as a medium of exchange and

become willing to buy it, they create the very conditions required of it

to make it more useful. There is nothing irrational, therefore, in

treating Bitcoin’s price as the cause of its value and no reason to

expect the momentum in its exponential upward trend to cease.1

prophesy: as more people believe in it as a medium of exchange and

become willing to buy it, they create the very conditions required of it

to make it more useful. There is nothing irrational, therefore, in

treating Bitcoin’s price as the cause of its value and no reason to

expect the momentum in its exponential upward trend to cease.1

Conclusion

Every time you buy Bitcoin, a fairy gets its wings. Now clap your

hands, click your heels together three times, and believe in Bitcoin! It

will only take faith the size of a mustard seed.

hands, click your heels together three times, and believe in Bitcoin! It

will only take faith the size of a mustard seed.

-

This analysis leaves something to explain—if the value of a medium of

exchange is just the market cap, why does Bitcoin go through hype

cycles? Every time Bitcoin goes up in price, that is an increase in its

underlying value, so why does its price ever crash? I don’t know the

answer, but I think I have a reasonable hypothesis: the network takes

time to adjust to the enormous number of newcomers during each hype

cycle. Each member of the network adds value, but this takes time—the

members of the network must learn something about one another before the

value they add to the network is more fully realized. If this effect is

real, then the price could temporarily rise more rapidly than the

growth that the network can support.

Open your free digital wallet here to store your cryptocurrencies in a safe place.