Under the microscope: conclusions on the costs of Bitcoin

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Bitcoin: Education can make a difference

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Bitcoin: the future of payments

Payments networks revisioned with bitcoin

Why bitcoin is held back

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Bitcoin vs. banking: an infographic

That’s not the only infographics that the people over at Visual Capitalist have made regarding the subject of Bitcoin. Back in February of this year Visual Capitalist released an infographic entitled, “The Definitive History of Bitcoin” which explores the history of Bitcoin ranging from; the Bitcoin design paper by Satoshi Nakamoto that was published back in October of 2008, the first real transaction with bitcoins, the rise and downfall of Mt.Gox, and ends in December when China announced they would not allow banks to handle bitcoins.

That’s not the only infographics that the people over at Visual Capitalist have made regarding the subject of Bitcoin. Back in February of this year Visual Capitalist released an infographic entitled, “The Definitive History of Bitcoin” which explores the history of Bitcoin ranging from; the Bitcoin design paper by Satoshi Nakamoto that was published back in October of 2008, the first real transaction with bitcoins, the rise and downfall of Mt.Gox, and ends in December when China announced they would not allow banks to handle bitcoins.

Open your free digital wallet here to store your cryptocurrencies in a safe place.

How the Bitcoin landscape is evolving in 2014

(CoinDesk) Like any new industry, there are so many areas to explore in the bitcoin space that sometimes make a week’s worth of developmentsit feel like a month or two have gone by.

1. Big-name retailers jumping on board

2. A warming regulatory climate

3. VC firms keep betting big

4. Building on the block chain

5. New emphasis on transparency

Open your free digital wallet here to store your cryptocurrencies in a safe place.

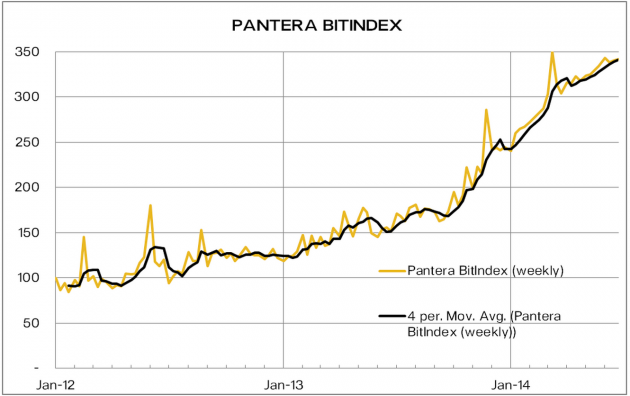

Pantera Launches BitIndex to Track Bitcoin

Components of index

- Developer interest on GitHub.

- Merchant adoption as a measure of consumer adoption.

- Wikipedia views measuring bitcoin education.

- Hashrate by logarithmic scale corresponding to orders of magnitude.

- Google searches captured by the number of times “bitcoin” appears.

- User adoption as measured by wallets.

- Transaction volume on the bitcoin network.

Always about price

Focus on investing

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Polish Finance Ministry says Bitcoin can be used as financial instrument

document confirming that under the country’s existing financial

regulations, bitcoin can be considered a financial instrument.

opposition member of Parliament for the liberal Twoj Ruch (Your

Movement) party. At the time, Pacholski asked Poland’s Ministry of

Finance to explain the legal status of bitcoin transactions.

Specifically, his query focused on whether or not “options and futures

contracts can be considered as a financial instrument” if they are

denominated in a digital currency.

“Options or futures contracts which are based on

[bitcoin] as a base instrument can be considered as derivative

instruments, and as such, they can be considered as financial

instruments, according to the bill on financial instruments.”

Bitcoin’s legal status clarified

recognized currency in Poland. He said in the policy document:

“An analysis of national regulations allows to conclude

that bitcoin … is not a legally defined and universally accepted

currency, because it cannot be classified as either a national currency …

or a foreign currency.”

possibility of issuing options and futures contracts in the form of

derivatives based on bitcoin market indexes. These issuances, he said,

would be similar to the derivatives which are based on stock market

indexes.

available to Polish investors. This, the Finance Ministry said, is in

accordance with the country’s banking services regulations.

Regulators accept bitcoin usage

derivatives markets suggests the continued evolution of government

policy toward digital currencies in Poland. While bitcoin can be used as

a medium of exchange and financial tool, it remains unrecognized as a

legal currency by regulators.

Szymon Wozniak, a Finance Ministry representative, said that the

ministry does not consider bitcoin to be illegal, but it does not

consider it to be a legal currency either. He remarked:

“What is not forbidden is permitted. However, we certainly cannot consider bitcoin to be a legal currency.”

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Bitcoin history: pre-blockchain digital currencies

(CoinTelegraph) For anyone not involved in

mid-90s cypherpunk scenes or early e-cash projects, the term “digital

currency” probably never came up in conversation until quite recently,

after the advent of Bitcoin.

But Satoshi’s white paper

did not invent digital money; that’s an idea as old as mainstream

internet usage itself. Bitcoin, and the altcoins it spawned, just

happened to be so revolutionary that all those electronic currencies

pre-2009https://holytransaction.com/page/before-bitcoin get overshadowed.

It’s like the Christian calendar. There is before-Bitcoin (BB), and then there is the current era, (AB).

Let’s take a look at some pre-Bitcoin technologies to get an idea of how far cryptocurrencies have come since.

1990: DigiCash

In 1982, cryptographer David Chaum applied the idea of blind signatures to money in his paper “Blind Signature for Untraceable Payments.”

Eight years later, he took these cryptographic protocols to market with

DigiCash, a company that ultimately went bankrupt in 1998.

1996: E-Gold

E-Gold sounded like a fine idea at the time: Create an account, send

in your gold or silver, and your accounted would be credited. Those

credits could then be easily transferred among accounts. The company

slowly built a successful operation through the late 90s.

By 2001, E-Gold was running into problems, however. The US Patriot

Act, first of all, tightened regulations on businesses that could be

classified as money transmitters. Gaining money transmitter licenses for

all 50 states proved too big of a hassle for E-Gold and its

competitors.

Furthermore, a campaign began to grow against E-Gold that marked it

as the currency of money launderers and child pornographers. A federal

indictment followed in 2005, which marked the end of E-Gold as a

meaningful alternative currency.

1998: Beenz.com

Beenz was a currency created to incentivize behavior such as visiting

specific websites, logging on through specific ISPs or shopping at

certain stores. This was back before the dot-com bubble burst, when

bored teenagers could take online quizzes, and marketing companies would

send them free stuff in the mail.

But the fetten Jahren ran their course, and Beenz.com was gone by 2001.

1999: Flooz.com

Flooz had a similar name and similar model to Beenz: Users were

rewarded for activity with flooz, which served as a medium of exchange

among its network of partners. Like Beenz, also, Flooz went bust in the

dot-com crash.

1999: InternetCash.com

InterenetCash.com filed a number of patents to protect its monetary

system based on prepaid cards, and it also relied on a network of

participating merchants where that cash could be redeemed. The company

ultimately raised $10 million in funding and had a staff of about 70

employees before the dot-com crash forced the company to close in August

2001.

After 2001, when economic realities hit many internet startups hard,

digital money never really caught on again, beyond some niche users,

until Nakamoto published the Bitcoin white paper in 2008. Of course, it

took a few years for most of us in the cryptocurrency community to catch

on, at which point cryptocurrencies took off far beyond what their

predecessors did.

We asked some community experts what present feature or

present reality in cryptocurrency tech today we will find funny and

old-fashioned in 15 years or so?

Aleksey Bragin:

“So many useless (or sometimes funny, as DogeCoin for example) alt

cryptocurrency clones emerged so quickly. That would go out of fashion

quicker than within 15 years, I suppose.”

Gideon Gallasch (coinsulting.eu): “I think mining – so much power and electricity is not sustainable long term.”

Lech Wilczyński (Co-Founder/CEO / Developer at InPay S.A.): “Centralized exchanges.”

J. Ryan Conley (CEO & Founder at Ryan Conley

Marketing & Training and CEO & Founder at Team Extreme

Worldwide): “That the banks were last to catch on to this awesome

concept! Staged viral video marketing platform.”

Patrick Dugan (CIO of Crypto Currency Concepts): “Centralized exchanges for sure, mining possibly.”

Lech Wilczyński (InPay.pl): “Bitcoin payment gateway.”

Open your free digital wallet here to store your cryptocurrencies in a safe place.

New Zealand central banker: cryptocurrencies could supplant cash

Advantages and drawbacks

“[Bitcoin] is a very low cost payment method with strong security features and usable for cross-border transactions, making it advantageous in some regards relative to more traditional payment mechanisms.”

“Key attributes of trust (that the ‘money’ gives rise to settlement of the obligation) and anonymity (it is often efficient for the sale/purchase parties not to have to identify one another) must be met, but if these can be accomplished reliably and sustainably, new technologies could supplant cash as we know it in years to come.”

Banks need to keep up

Apart from the carefully worded statement, regulators have taken any measures to curb or control the development of the bitcoin economy in the region.

Open your free digital wallet here to store your cryptocurrencies in a safe place.

Why Bitcoin may re-write banking practice

(BusinessTech) Bitcoin has grown from an experiment in digital cash to a vibrant, global economy supporting multi-million dollar companies with a market cap of $10 billion.

“While the road has been bumpy, and quite a rollercoaster ride, it is still nascent and holds immense promise to change the world in unprecedented ways,” said Simon de la Rouviere, speaking at the recent Nedgroup Investments Cash Solutions Treasurers Conference.

“In 2013, the hockey-stick growth often found in the technology space kicked off for Bitcoin, seeing adoption increase worldwide.” De la Rouviere, a technology entrepreneur who develops cryptocurrency applications, believes that Bitcoin’s global, public, distributed asset ledger is a fundamental innovation that could upset various industries – from banking to public records. “Any business in the field of recording information fit into a ledger that charges fees to be a middleman is at risk of becoming obsolete,” he said. As copy of Bitcoin’s ledger exists on every network participant’s computer, and is continually updated, reconciled and synchronized in real-time. Each member can make entries into the ledger, which records transactions of a certain amount of currency from one participant to another. Each entry is propagated to the network, so that every copy on every computer is updated near simultaneously and all copies of the ledger remain synchronized. “This blockchain technology could easily be adopted to work with title deeds, physical keys, private equity, derivatives, escrow, dispute mediation, passports, wills, domain names, and sim cards – to name but a few,” De la Rouviere said.

The future

Looking farther ahead, the technology could potentially bring about a new apolitical reserve currency that allows programs and machines to own forms of value without the requirement of human intervention.

This could herald an almost sci-fi era, where machines earn their keep by providing services to humanity at an even more cost-efficient, break-even level than currently possible, De la Rouviere said.

“By thinking of Bitcoin not as a currency, but as a single solution to a previously unsolved algorithmic problem in distributed systems, colloquially known as the Byzantine Fault Tolerance, humanity can create global systems of consensus powered by mathematics.” Bitcoin is a grand experiment, currently at the forefront of showing the equalizing force that the internet brought about. “It might still one day fail,” he added, “but rest assured, it is spurring innovative thinking across the board.” Sean Segar, head of cash solutions at Nedgroup Investments, said that while the bank believes in staying abreast of trends or fads that may affect the industry, “we have no plans to launch a Bitcoin fund”.

Open your free digital wallet here to store your cryptocurrencies in a safe place.